At TravelCon, Matt presented on risk and savings when he purchased his refrigerator using a combination of gift cards purchased from the local grocery store + fuel perks or using Raise to purchase discounted gift cards with TopCashBack savings.

The line segment of $45 and $193 is the method that Matt pursued, using a 5% card and purchasing gift cards at the local grocery store with a bonus fuel rewards. The flat $145 savings is purchasing the gift card discounted on Raise with a 2% cash back.

The reason why you could wind up with $193 or $45 is because the fuel rewards have limitations: you would need to be able to buy the maximum fuel and work around the expiration date. If you don’t fully utilize, you could wind up as low as the low $45 savings.

As you can see from the slide, your risk premium is $48 as that is the difference between the max, $193 and the $145, the simplest way towards savings.

At the end of the day, your opportunity is how you are able to maximize it, if you can’t and choose the wrong option, in this example, you will be left with $45.

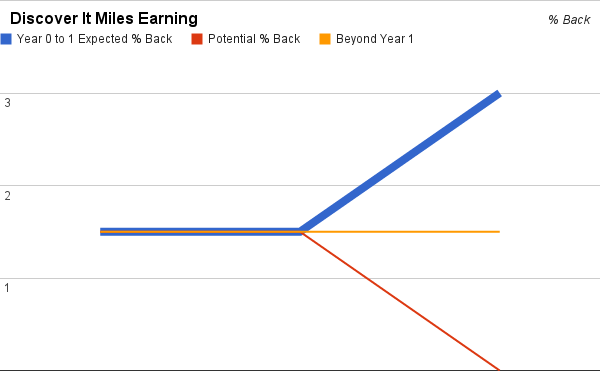

Discover It Miles

Doctor of Credit has a great review of the newest Discover It Miles card. Here’s the summary of the earning side of the card:

- For every $1 spent, you will receive 1.5 miles

- As the sign up bonus, after 12 months, you will receive a bonus equal to the total amount of miles earned

{kind=link}

Now we look at this chart, everything starts at 1.5% back. The blue line represents year 0 to 1 where you could effectively double your spend at 3%. However, what happens if Discover thinks you’re abusing the card? They’d close your card and your earnings could be like the red line, 1.5% to start then 0%. Even if you don’t get shut down, they could throttle you and put your account under review. You’d still receive the extra 1.5%, but is it worth it?

My Thoughts

It never crossed my mind to even think of the Discover It Miles card like this until Matt’s presentation at TravelCon. Without a doubt, yes if you play by Discover’s rules, you could earn 3% on all of your spend on the new signup for the first year. But if you start coloring outside the lines, well, what will be your earnings? For all intents and purposes, yes the card is a 3% for the first year, but the for folks that read any manufactured spending blog it should be “Discover It Miles, earn 3%* in your first year” with a footnote that you might wind up with less 1.5%, especially if they decide to take away your final months’ miles.

I hope you all have the same opportunity and experience to listen to a presentation from Matt, it was quite a lesson.

It should also be noted that using GCs eliminates the extended warranty that would have come with (most) credit cards. I often choose full cc payment on products like appliances and electronics to catch the extended warranty. A second type of risk to be considered…

Risk is great, it allows people to offer you a reward in order to compensate for it. In this example you would just calculate the cost of the warranty and then decide if the present day reward is worth it.

Damn, I was just thinking of writing up on MSing with Discover Miles for a Manufactured Monday post. Oh well, maybe I’ll write about it anyway. We’ll see…

It was a nice post!

But what about the time/value of that additional 1.5 miles for the Discover Miles card? Generally, miles, like money, are more valuable now than in the future. However, one could argue that if Discover moves toward creating a transferable currency (a la Citi TYPs, Chase UR, AMEX MR, etc), then that additional 1.5x could actually be more valuable. The problem is, the opposite could be true – they could devalue the program before you receive the miles, and therefore can burn them.

I guess I’m getting at – Matt properly reflects much of the risk, but is there more out there that we’re not really considering? It could just be me trying to get up to speed on the Discover Miles card/program–which to me, seems similar to a cashback program at the moment, without any transfer partners.

Yea the Discover IT Miles just seems to be a 3% cashback card at this time. Would love to see the “miles” transferable to different programs. My fear for everyone is if the huge influx of people sign up and MS hard, and it’s like the reports in the Forum about the Diner’s Club card where it’s not worth the trouble