Credit Card Shutdowns

As documented by Miles Per Day, Vinh has posted several credit card shutdowns from various readers as data points. The shut downs were all across the board, from too many credit cards to huge ramp up in spend to getting shut down and then getting their cards back among other stories.

However, because of our nature of being knee deep into manufactured spending we think that is the culprit. But really. Is it? We need to pause for a moment, zoom out a bit, and think at a more macro level. At a higher level, it might not be manufactured spending after all. There’s a bigger movement out there if you dive deeper into the industry as a whole.

Other Shutdown Factors

We’ll start with the obvious one that’s plastered all over the media today. Bitcoin.

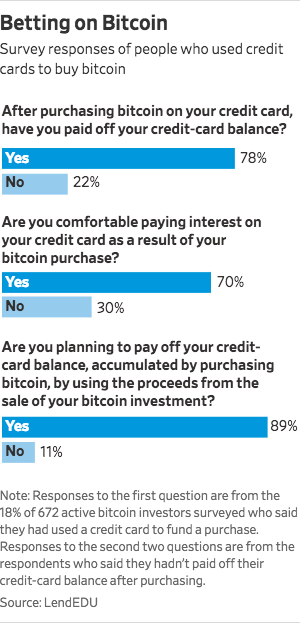

Buying bitcoin is a risky proposition. There’s wild swings and what happens if you bought it at the peak in December on credit card? Look at the price today. Bitcoin would be underwater and how would someone pay for that on their credit card? Especially if they maxed out the credit card? Vinh already reported that. Banks like Capital One, Discover, and TD are blocking bitcoin purchases. Maxing out your credit card buying bitcoin is asking for trouble. I once met Matt on Saverocity (note the distinction, Matt on Saverocity not Matt @Saverocity himself) in NYC and he told me a story from FatWallet. The basic premise was a guy loaded up his credit cards buying gold and declared bankruptcy. Guess what? You can do that too with bitcoin. How risky is that for the banks? Super risky.

What will people do who carry a balance holding bitcoin when the cryptocurrency has a wild swing? Banks love their interest when people fall behind on payments, but not so much when it becomes too risky. Best to shut folks down before they get out of hand. From WSJ:

Investors need to cover what often are double-digit interest rates on credit cards if they don’t pay the bill in full, in addition to fees on the bitcoin transactions. To offset those costs, borrowers need bitcoin to rise substantially in value. That can increase the chances of borrowers not paying their credit-card bills if they owe more on the asset than it is worth.

…

Fraud losses are also a concern for card issuers. As more cryptocurrency exchanges emerge, some card companies say there is an elevated risk of consumers purchasing bitcoin from a fraudulent exchange. Card holders typically aren’t responsible for fraudulent purchases charged to their credit card, raising the risk that card issuers could be stuck with the loss.

…

Card companies have also cited worries around the lack of transparency with bitcoin purchases that could subject them to legal risk around anti-money-laundering obligations. That can include concerns that the seller of the item is using the funds for illegal activities.

“There’s a host of issues,” said David Nelms, Discover’s CEO. Among others, “we don’t want to be responsible if someone buys bitcoin and it drops 50% the next day.”

It wouldn’t surprise me that banks are now very fearful of people buying general purpose gift cards to load up on bitcoin. Citi used to not care unless you were doing something crazy.

The No Surprise For Shutdowns

Throughout 2017, personal credit card debt has been rising and is probably over $1 trillion today. Delinquency rates are increasing. In September 2017, the Wall Street Journal covered this topic.

At Capital One, loans over 30 days delinquent in its domestic credit card portfolio ticked up to 4% of total loans in August, from 3.5% in April, monthly data from the company shows. Over the same period, this ratio rose to 4.5% from 4.1% at Synchrony, and to 5.3% from 4.7% at Alliance Data.

…

The market didn’t react much to the monthly numbers, which were released Friday. But shares of Capital One, Synchrony and Alliance Data are down 7%, 19% and 5% respectively this year.

…

Credit problems are creeping up, he said, because consumer debt has been rising faster than incomes. Seeing this, Capital One began slowing its lending growth last year, having “surged with growth” in 2014 and 2015.

Capital One has twice raised its guidance for defaults it expects in 2017, denting confidence in the company’s forecasts. Investors declined to grant Mr. Fairbank a vote of confidence even while he was on stage at the Barclays conference—a poll of investors in the audience found that 60% expect defaults this year to exceed 5%, which is what the company is currently predicting.

After reading that, does it surprise you that someone got their Capital One card closed? Not any more, right? AMEX is setting aside close to $1 billion for bad loans. The trend is there with loans going sour.

3 Easy Steps To Fix That

- Stop the appearance of risky activity.

- Incorporate and move spend onto a business credit card.

- If you continue to use the personal cards, use a realistic amount of credit. Don’t ramp up the cards so high. There’s no need to do that.

Buying bitcoin is a form of MS for many

It wouldn’t surprise me! I think there’s safer ways for MS for both as the MS’er and the banks

Not seeing the connection here. People MS for months, sometimes years before being shut down. During this time the usual MSer could consistently pays off their bill, often before it cuts. That’s the opposite of a risky pattern.

Right, it’s just now it’s more risky than ever for the banks. Delinquencies are up, which I think is the biggest reason. It’s hard for one bank to see the full picture with 100% credit limit utilization in a 5 digit credit line pay off before it’s all due. I used to buy so many gift cards and use one card to pay off another card. The quick cycles is that you could do balance transfers all over the place and rack it up somewhere. Then at the end of the day you could be like the gold story, where you declare bankruptcy and hold thousands in some cryptocurrency that the banks can’t reclaim to pay defaulted debt

Agree that consumer debt load is rising faster than income and that banks are gearing up for a bumper crop of defaults. The trigger should be when the Fed start serious interest rate increases, but the banks no doubt have rigged up their analytic trip wires to make preemptive strikes before then.

This is where I am nervous. I have very high balances on several cards carried over month to month because of free balance transfers all on personal cards