Last week, I wrote about my plan for a price match and how it didn’t quite go the way I wanted it to. Today, I want to let you know about my experience with a new credit card.

A couple of weeks ago, I applied for the Best Buy credit card to play around with the gift card churning opportunity. I was hoping to also grab some good offers like my buddy @ Personal Finance Digest. He’s got quite a few links regarding extra opportunities using the Best Buy credit card that are a must read.

When I signed up for the card, they wanted me to call them to verify my personal identifiable information. After completing the call, I was approved with a $4,000 credit limit. I thought this was perfect. After hearing $4,000 limit, I didn’t think much of it. A couple days later I received a letter stating I was not approved for the Best Buy MasterCard! Instead, I was approved for a Best Buy only store card.

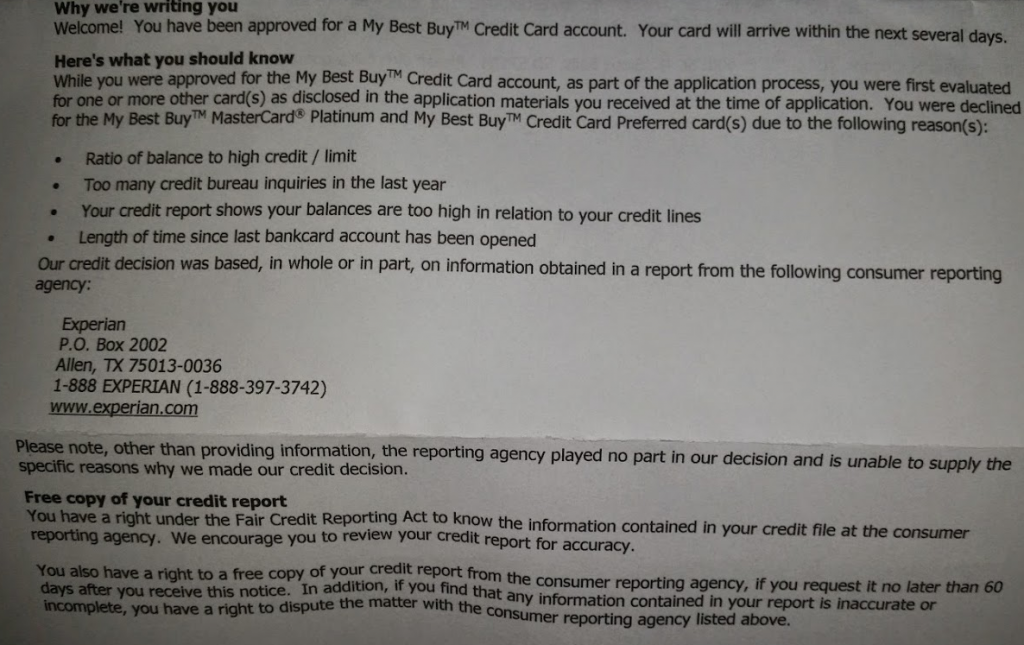

So apparently, the four reasons they declined me were:

- Ratio of balance to high credit / limit

- Too many credit bureau inquiries in the last year

- Your credit report shows your balances are too high in relation to your credit lines

- Length of time since last bankcard account has been opened

Oops on the first and third bullet. I let a statement close very close to utilizing the entire credit limit, which was completely paid off. I did not let the next statement close to have it reported to the credit bureau’s.

While I wanted the Best Buy MasterCard, I’m actually glad I wasn’t approved for the MasterCards if they didn’t think my creditworthiness was good. This isn’t your normal US Bank lower product which the sign up offer is lessor or Bank of America Alaska Airlines 5,000 miles offer.

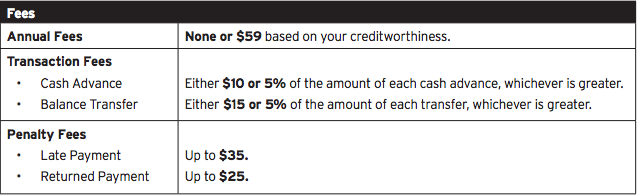

The My Best Buy Credit Card could have a $59 annual fee!

If I’m going to pay $59 for an annual fee, it sure as heck isn’t going to be a Best Buy credit card! The good thing about this credit card is it virtually is the same as a MasterCard in terms of its benefits. I’ll be testing it further and seeing if its worth while. Another good thing about the credit card, it’s issued by CitiBank, if I don’t like it enough, I hope there’s the ability to product change it into a Dividend card.

Citi’s tightening up on credit? Wow!

Yep! Surprised me too. The plus side – this card can be paid on Evolve. Not sure if it can be said about the Mastercard version

As you say, this may be a blessing in disguise. It can be hard to get *just* the store card these days. I applied for a Gap card a couple years ago, and there was no way for them to specify that I didn’t want the visa, but just the Gap store card. She said I could call in and downgrade once I had it, but I never bothered. No AF on the Gap card, though.

Yep, could be a blessing – so far, I’m getting all the bennies of the Mastercard and ability to pay on Evolve

Hi,

I was trying to downgrade one of my CITI-EX cards to a non-paying product and the agent mentioned that it’s a hard pull…I just started a churn at the end of the December and my annual fee is due in Feb…Does it make sense to downgrade to a DIVIDEND and take the score hit?

That is very interesting! I checked Credit Karma and didn’t see any hard pulls.

Have you checked out this thread? Maybe some of the other folks that commented can provide better advice.

http://saverocity.com/miles4more/downgrade-citi-card/

For me, I think it’s a great way to keep your average age of accounts, and the 5% cash back quarterly categories is great.

I don’t think citi will let you convert to a cc. retail is probably a completely separate division. Though it might count for the limit of how many citi cards you can apply for in a certain time frame (I am unclear on how long). An advantage if it being citi though is you probably can pay with debit card over the phone (I’ve done that with my staples account, which is also citi.)

I will definitely be trying the debit card over the phone as soon as the statement closes. I’ll update next year to see if we can do a product change, but you are right with different divisions and will probably be next to impossible.

Banks report account balances to the credit bureaus an a set day each month (this varies by bank, credit bureau (and often by state)).. The day your statement closes and the open balance at that time are, unfortunately, not relevant to your open balance reported the bank on that day. Not factoring in statement closing date overstates the creditors risk, in my opinion, as this overstates the credit utilization ratio on all cardholders who pay balances in full on or before statement close

Definitely a mistake in that I should have planned better and paying the bill earlier instead of letting it stew with it being reported into the bureaus