IF YOU HAVE EXTRA MONEY, DUKE ENERGY WOULD LIKE SOME OF IT: We don’t even remember how, but in the course of our internet wanderings we came upon this page promoting something called Duke Energy PremierNotes. This is a utility company offering consumers something like a money market account or checking account, except not as good, and you should stay far, far away from it.

There are two things you need to know about PremierNotes:

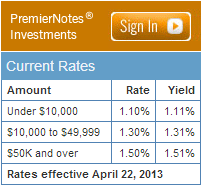

- They offer slightly higher rates than you can get from a savings account.

- They are not FDIC-insured.

Obviously there’s nothing wrong per se with investments which are not insured by the FDIC. The question is, does the additional reward offset the risk? How much higher are the rates on this investment vehicle vs. other liquid accounts?

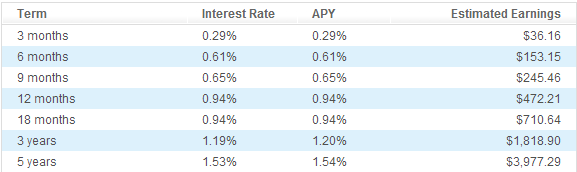

That’s not very high. By way of comparison, here are the CD rates at Ally Bank:

Note that if you pull your money out of the Ally CD before it matures, the penalty is only 60 days’ interest. So at Ally, you’re making an equivalent interest rate AND you’re federally insured AND there’s not a $50,000 minimum.

Note that if you pull your money out of the Ally CD before it matures, the penalty is only 60 days’ interest. So at Ally, you’re making an equivalent interest rate AND you’re federally insured AND there’s not a $50,000 minimum.

How risky is Duke Energy? As per their investor page, Fitch has them at BBB+, Moody’s has them at Baa2, and S&P has them at BBB+. In other words, they are just above a junk bond rating. If you want to invest in junk bonds, then invest in junk bonds–but do so by actually buying the bonds, preferably via a low-cost index fund or an ETF so that you’ll diversify your risk. Your rate of return should be several percentage points higher that the meager gruel served up by Duke Energy.

The Duke Energy PremierNotes pay you much, much less than they ought to given the level of risk you’re assuming. Why do they offer this product? Because they can. Because people without the inclination or the ability to think about their investments hand over their money to a trusted name.

What people are investing in this awful product, you ask? We’re not sure, but we did notice that Duke Energy PremierNotes has an “Employees and Retirees” page. According to BusinessWeek:

“I like to call them a bond with a checkbook,” said John Heffernan, director of the PremierNotes program at Duke Energy. “The unique thing about this is we’re selling them directly to the investors.”

Duke Energy started offering floating-rate notes to individuals about a year ago [Ed: this article is from June 2012], marketing them first to employees and through billing inserts to customers before advertising in newspapers, Heffernan said in an interview. The amount of debt outstanding through the program increased 59 percent to $126 million as of March 31.

$126 million! Odds are they won’t lose their money, but… it’s not worth the risk. Shame on you for offering this product, Duke Energy.

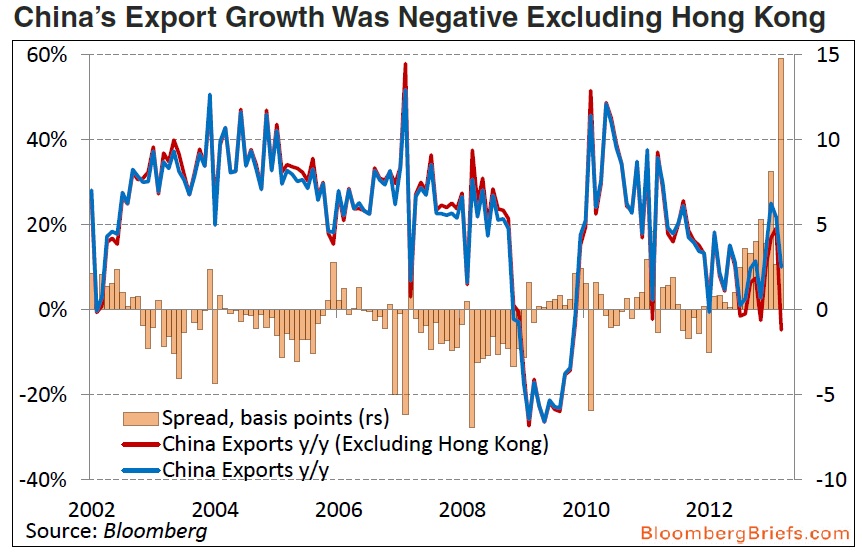

CHINA EXPORTS DECLINING: An interesting graph from Caitlyn at The Big Picture:

An explanation of what’s going on here:

China’s external sector is probably expanding much more slowly than overall export growth implies. Have a look at “unusual surges” in China’s “reported shipments to Hong Kong.” It seems the entire country is either channel stuffing or dumping goods or ever cooking books via inflated invoices. Another thesis is that Exporters are “repatriating capital through export transactions rather than through traditional methods” to avoid Mainland’s controls and/or taxes.

As Bloomberg Brief points out,

Chinese exports to Hong Kong jumped 93 percent year-on-year in March, while annual growth has averaged more than 50 percent since September. Hong Kong now accounts for 27 percent of China’s total monthly ex-ports, compared with less than 16 percent prior to September. None of China’s other major trading partners saw growth of this magnitude.

Odd stuff going on over there…

ONE LAST THING BEFORE WE LEAVE: Enter the code 10APRIL for $10 off a $100 order at homedepot.com (H/T: Slickdeals).

You’ve got Duke Notes completely wrong. It’s a completely loquid investment. Money can be withdrawn at any time. Ally banj does have FDIC insurance but they are one of three banks to fail the stress test. If you consider the modest early withdrawal penalties at Ally Bank, the Duke Notes give a superior completely liquid return. Duke is not going bankrupt! The jury is still out with Ally because of the incredible support they still receive from the Federal Government. I won’t bank with them.

Shame on you for being a shill for Ally.

Bob–very silly comment. No insurance + low rate of return = bad idea.

As far as me being a shill for Ally: I wish! I’ve never seen a cent from Ally, alas.

Question: how much do you have invested in Duke’s shitty product?

Your argument is ludicrous and poorly formed. Rate differences between Ally and Duke is not differential equations, it is simple math. I can’t and won’t waste time explaining it to you. How you come to your conclusions??????

And, before you ask how ask how much I have invested in this “shitty” product, as you did above, please don’t further embarrass yourself. This is an over-the-top personal question and goes directly to you shoddy and loose thinking. As they say, “I can drive by that one ninety miles and hour and see all I need to see.”

You sir, should not be posting. In addition I don’t believe you are not shilling….Lastly fyi, I have a LOT

invested with Duke Notes.

about things in general……

is

Best of luck with your investment!

Over 2 years later and still no one has lost any money on this investment.

a couple of points:

ally only calculates interest on a monthly basis

FDIC does guarantee your money, but it never says when you will be paid. If a big bank run occurs, money in the FDIC will be paid to you but you have no guarantee of when. It can be years if the government has other priorities.

The following are not FDIC insured and if you invest, must be willing to lose it all if something goes really bad, however you will be paid prior to shareholders and yes you might not get $1 for $1.

ford interest advantage is also not FDIC insured but pay pretty well. Ford used to offer a 10 year note that paid 7%. That was really good.

Mercedes has probably the highest interest rate but you have to pass their credit worthiness ‘test’.

Duke is pretty good and currently paying a wonderful interest rate. I think the max investment is now 2 million dollars.

I see you have a disclaimer at the bottom that you are getting compensated for your posts.

1. This post was written many years ago.

2. I haven’t been compensated for a post in many years, and the small amount I did receive was for credit cards.

3. I received no compensation whatsoever for this post.

the nations largest electric utility is not going belly up….please. Note the word LARGEST . Your bank may be allowed to fail, there are many banks. Your broker may be allow to fail, there are many brokers. But when your flipping electricity stops coming into your house it gets everyones attention and pronto. I have held Duke stock since 1989, never sold single share and still buying every month. I have a large positions in the Notes as well. By the way the dividend yield is usually at 4.4% except when the stock price rises ( not the usual for a company failing ). PF just go away. Your name should be chicken little because you think the sky is falling. Stick to your CD’s and let inflation eat your lunch

It is five years and I am still going strong with Duke Notes, which is managed by the highly rated Northern Trust Bank. Right now I am getting 2.6% on my investment, all of which can be immediately transferred to my other banks anytime I want, and I can write a check anytime I want.

You can’t find a liquid account with or without check-writing with that rate.

This is a great investment grade product with the interest rate but without the holding period of other investment grade products. I would like to know if anyone knows about anything else like it.

The big lesson here is to spot the receptive posters and to call them out.

I have a ford bond that pays 7.75 until 2049 If I sell it I would have to pay capital gain tax

What happened to the good interest rate?