Disclosure: There are a billion credit card links in this article. None are my affiliate links.

This post is more for beginners but I also feel like it could be useful to others. Feel free to ignore though. Anyway, a little over week ago I wrote about the bigger Delta and United card bonuses that were out there (United’s dead, Delta’s dead in a day or two). Drew at Travel is Free wrote a great article complaining about the big bloggers pumping crappy cards for affiliate conversions; dissing the larger sign up bonus on the Delta card since Delta Skymiles are the worst currency out there. While I disagree with that particular point (I happen to enjoy finding Delta award space and also am doubling down on bit on Delta miles for travel next year, fingers crossed), there was a great point he made – you shouldn’t be wasting applications on cards like the Delta 50K card if you haven’t gotten the better cards out there first.

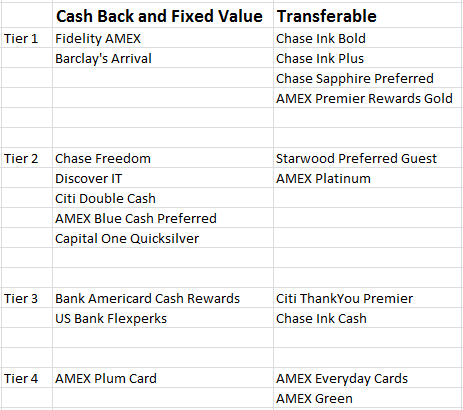

So what I’ve decided to do is put together a credit card rankings list – a tier list. I actually think this is a pretty useful exercise to help me make sure I’m recommending the right cards to friends and readers when they ask. I’ve split cards into four categories: Cash Back and Fixed Value Cards (where you use points essentially as cash for travel), Transferable Points, Airline Miles, and Hotel Points. Obviously there is some overlap on certain cards, I’ve placed them in the category in which I personally use them. I’m also a little rusty on Cash Back cards since I haven’t focused on them personally for awhile.

A couple of notes. I’ve decided to rank the cards based on my personal usage, which I think is similar to the usage of many of my friends. This chart is mostly geared towards people who mainly earn via sign up bonuses – with maybe a little bit of regular spending/manufactured spending on the side. If you’re familiar with Milenomics “traveler levels“, I’m more speaking to Level 201 (mostly domestic travel with one or two international trips sprinkled in per year).

These rankings are, obviously, purely my own opinion. Also, this is just a guideline, you have to look at the list through the lens of your own spending and flying patterns. I’d love to hear people’s thoughts as well – I think different perspectives are great for these kinds of things.

For each type of credit card, I’ve placed cards into four tiers. Tier 1 cards are cards that I think should be a part of every serious points enthusiast’s portfolio and Tier 2 cards are cards to start focusing on after you have most of the Tier 1s. For me, Tier 3 and Tier 4 cards are cards that you get once you’ve maxed out on the first two tiers or if you want them for a very specific purpose. Tier 4 cards are basically dead to me unless I am signing up for them in order to redeem their benefits immediately (within a year). But am I seriously going to start building a huge balance in Korean Skypass? Likely not.

Again, just my opinions! Here’s my list for Cash Back and Transferable Points cards (and obviously every card in existence is not on here, though I’ve tried to include as many of the “pimped” ones as I could).

How would I suggest you use this list? If you see a blogger advertising a credit card and it’s in one of the lower tiers – take pause, do some research, and think long and hard about it before you apply. I’m not saying Tier 3 and Tier 4 cards are useless, but most of them only have specific uses for specific situations. Make sure you have most of the Tier 1s and 2s or a very specific situation before you waste time with the other cards. I swear every 5 months my friend asks me if a 50K bonus on the Marriott card is good and I just keep repeating, “get the better Chase cards first.”

Here is some of the thinking that went into each card section. I’m gonna include sign up bonuses when applicable, like this (bonus/spend). For the fixed value card, even if you earn “points” I’m just going to give you the bonus in dollars. So a (40K/$2000) bonus means you need to spend $2000 to earn 40K points.

Cash Back and Fixed Value Cards

My general strategy for Cash Back and Fixed Value cards is to use them as default, non-bonus spending, or to use them for the light manufactured spending that I do. I don’t really recommend having more than a couple of these cards unless you are crazy MSing all the time.

The Tier 1 cards are the main players in my opinion – 2% back on all purchases (2.2 for Arrival but who’s counting?). Out of the two, I prefer the Fidelity AMEX because there is no annual fee and the cash is straight cash, homey. The Barclaycard Arrival Plus World MasterCard® ($440/$3000) has drawbacks – you can only redeem for travel and you need to MS a bunch to offset the $89 fee after the first year. You can read PFDigest’s analysis of these two cards here.

Chase Freedom ($100/$500) and DiscoverIT ($150/$750) are both fee free cards with rotating 5% bonus categories that can be very lucrative. The Amex Blue Cash Preferred ($150/$1000) has kind of lost its usefulness since the bonus categories are now capped and the annual fee remains $75, but it’s good for regular spending for a lot of folks so it makes Tier 2. The Capital One Quicksilver ($100/$500) gives a pretty decent 1.5% return for no annual fee, while the Citi Double Cash card might be annoying but if you can get the 2% back then obviously it’s a solid card.

Tier 3 features a couple of cards that I don’t personally own but might be useful to some in specific situations. The Bank Americard Cash Rewards card ($100/$500) offers 3/2/1 on gas/groc/everything (capped) for no annual fee while US Bank FlexPerks Travel Rewards Visa Signature ($200/$3500) gives you 2% on gas/grocery/airline and 1% on everything else for a $49 annual fee. It’s a bit complicated to redeem FlexPerks points hence the Tier 3 status.

I used the Plum Card as an example of a Tier 4 card – it is very, very niche. You can make a nice profit if you spend $30K in 3 months, but after that the card is essentially useless and you’ll want to cancel before the annual fee hits – so it’s not a “backbone” type of card.

Transferable Points Cards

Transferable points cards are the bread and butter of my travel strategy, so they mean a lot to me. Obviously all the different cards have different partners; I don’t have time to go through all of them here, though I’ll highlight some as we go along. Cards that also have the ability to redeem for cash back receive a slight bump in my mind – flexibility is king.

I have three Chase cards listed in Tier 1 – Chase Ink Bold (50K/$5000), Chase Ink Plus (50K/$5000), and Chase Sapphire Preferred (40K/$3000). In reality, you only need one of these cards at a time – having one will give you the ability to transfer your Ultimate Rewards points to transfer partners such as United and Singapore Airlines. Don’t get all three unless you’re some kind of crazy Staples reseller (to utilize the 5X at office supply stores). If you have to get only one, I’d apply for one of the Inks, but make sure you have a small business first. Otherwise the CSP is acceptable.

My other Tier 1 card here is the Amex Premier Rewards Gold card (25K/$2000). This comes with a big caveat – I only consider it a Tier 1 card if there is a sign up bonus of 50,000 points or greater. If there’s not one available, I’d wait. The same goes for the business version. Membership Rewards have a lot of useful transfer partners, though you have to pay fees on some of them (like Delta).

Some might be surprised I have the Starwood Preferred Guest card (25K/$5000) in Tier 2. This card is here because the sign up bonus is just meh. SPG does have the most transfer partners (including AA and Alaska) and you get 25K for every 20K SPG points you transfer, so it’s a really good card, but the sign up is so low it’s never on my must have list. If you want to spend heavily on this card, then you can feel free to bump it up to Tier 1. Business version available as well.

The AMEX Platinum (40K/$3000) is in Tier 2 because although it has a ton of benefits, the high annual fee ($450) is a big barrier to entry. However, if you get a 100K bonus offer (make sure you read the terms and conditions to double check that you qualify), you can also bump this right up to Tier 1. There have been rumors of some of these big offers floating around for small businesses, check your snail mail. At its regular sign up bonus levels though it’s not a great card, even if you travel a ton, which is why the Gold version tops it in my book.

In Tier 3 I placed the no fee Chase Ink Cash, grab one if you’re desperate for a quick sign up bonus. No annual fee means you can keep it, though that will only benefit your business’ credit not your own. The Citi ThankYou Premier (50K/$5000 but over two years including an annual fee) is a new player in the transferable points game, but I just think their partners are a bit too niche to highly recommend the card right now.

Finally, the AMEX Everyday cards are pretty much junk, unless you need to keep your Membership Rewards points active – not even gonna bother with a link. I mean I guess they’re okay in some circumstances, but I have little to no interest in these guys. The Green card has no sign up bonus and generally feels kind of useless.

Final Thoughts

I worked on these lists because although I do it all the time, I believe applying for credit cards is serious business that should not be taken lightly. You should really have a strategy when you are applying for cards and part of that strategy is knowing which cards are better (so you don’t “waste” applications or spending bonuses). There’s a lot more strategy involved and you also need to balance how many cards you apply for at a time and to which bank etc. etc. So please think carefully before you decide to apply for cards, have a plan in place, and for the love of all that is good do not apply for credit cards if you can’t pay the balance off in full every month. Hopefully these tier lists help you to get your thinking process started.

Now, have at my tier lists in the comments! I plan on using your help to update and refine them!

Up next I’ll share my tier lists for Airline and Hotel cards – this post is too long already…

I like the way you categorized the cards. Nice analysis as usual.

I am traveling so only skimmed it but I am marking it for later! Thanks!

I’m curious, what are your leading cards for spend on Groceries and Gas? The Chase Sapphire Preferred still appears to be a leader for Restaurant and non-airline travel, but for many folks gas and groceries are the other two largest ‘everyday’ expenses.

Is there a leading card for bonus multipliers in those categories. (Particularly since you mentioned you hate the Amex Everyday Cards).

I think if you’re just using it for regular expenditures, the Amex Blue Preferred is the way to go – it’s 6% groc up to $6000 of spending and 3% gas. The reason it’s fallen out of vogue is it’s not as lucrative to MS anymore (due to the spending cap). The no fee version is 3%/2%. Both I think are better than the Everyday cards if you’re focused on Cash Back. I probably was a little too harsh on Everyday…might need to update later

Makes sense. I currently have an Amex Everyday Preferred because I was having trouble finding a card with bonus multipliers for groceries & gas; and I wanted something that would allow me to use and keep active my AMEX membership rewards points after I cancel my Platinum Card.

The Blue Cash Preferred looks like it’s solidly a better option. I couldn’t determine if like w/Chase you need an active full Membership Rewards earning card to use/transfer your Membership Rewards points?