![]() Today I pulled the trigger and opened a Vanguard ROTH IRA. The contribution deadline for 2013 is April 15th 2014, so if you move quickly you can open one up and fund for last year. After which, you can always fund the current year until that April 15th date every year.

Today I pulled the trigger and opened a Vanguard ROTH IRA. The contribution deadline for 2013 is April 15th 2014, so if you move quickly you can open one up and fund for last year. After which, you can always fund the current year until that April 15th date every year.

The process itself is quite easy and can be done fully online and should have taken me about 10 minutes to complete, however there were a couple of bumps on the way that I wanted to ask a human about so I didn’t make any mistakes in structuring the account.

Please note, if you decide to fund via Bank Transfer then you need the funds available today and the process creates a time stamp that shows your account open within the deadline, even though it might take a couple of days for the funds to show up on the other end. If you chose to fund via a check then you need to ensure that the letter is postmarked before April 15th (so they told me) but I didn’t trust that method so went for Online Funding.

Vanguard has a great reputation in the market as being the innovator behind Index Funds, these are low cost funds that track the market, and instead of having a Fund Manager actively selecting which stocks go into the fund they reduce costs by buying an entire Index or Sector. During the set up process I called up Vanguard Concierge to help answer a few questions, and I learned some interesting things about Vanguard that I wasn’t aware of, and you should be too. I’ll address them at the end of this article.

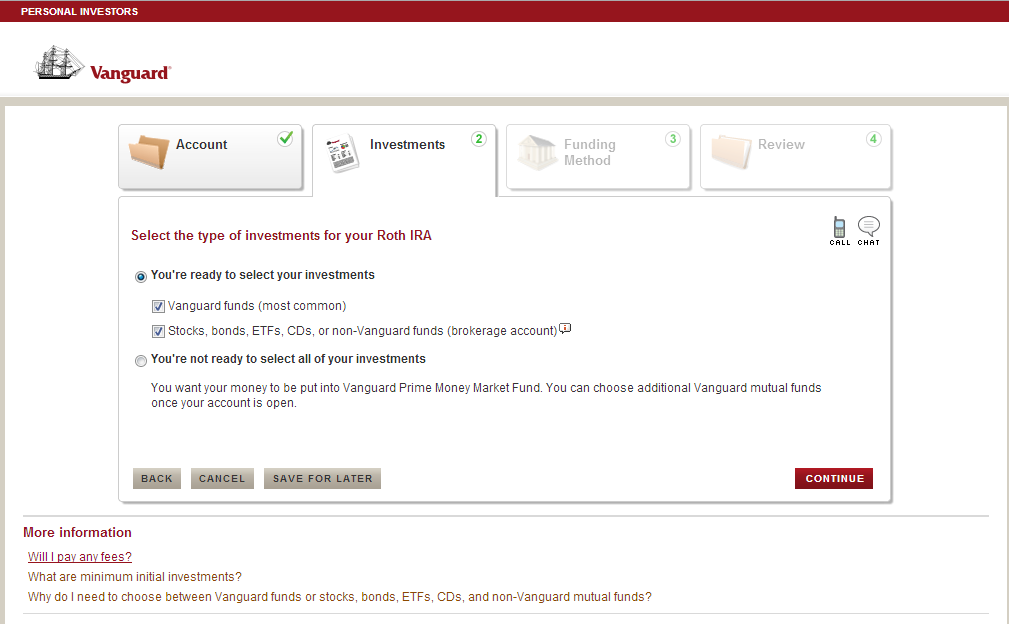

Opening a new Vanguard Account to hold the ROTH IRA is very simple:

Decide if you will be using this account to trade Vanguard Funds only, or if you also want to trade non Vanguard funds, ETFs and Equities

If you don’t select both options then you can always add on the Brokerage capabilities later, however if you do want to immediately fund these types of product then you best checking both boxes.

Fees – Vanguard will not charge you a fee if you sign up for Electronic Statements, otherwise there is a $20 annual fee for accounts with a balance under $10,000. Since I will be opening two accounts for $5,000 each I am signing up for the statements, plus I actually prefer them online along with it being better for the Environment.

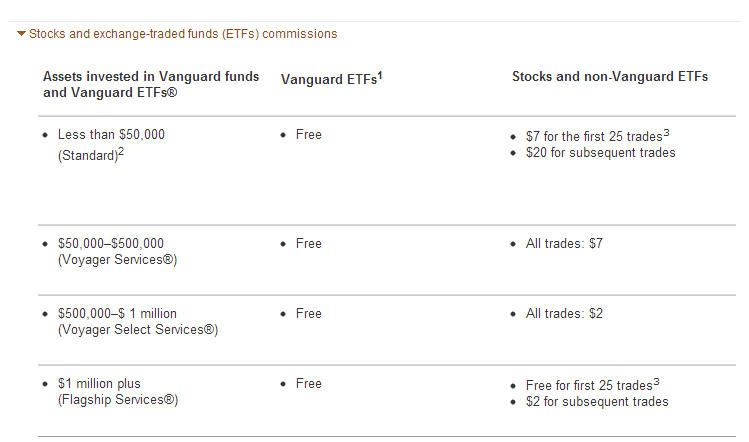

Brokerage Fees

For the Brokerage side of things, Vanguard charges a fee per trade, the starting rate is $7, but they don’t like a lot of active traders and penalize you for trading too much on lower balanced accounts

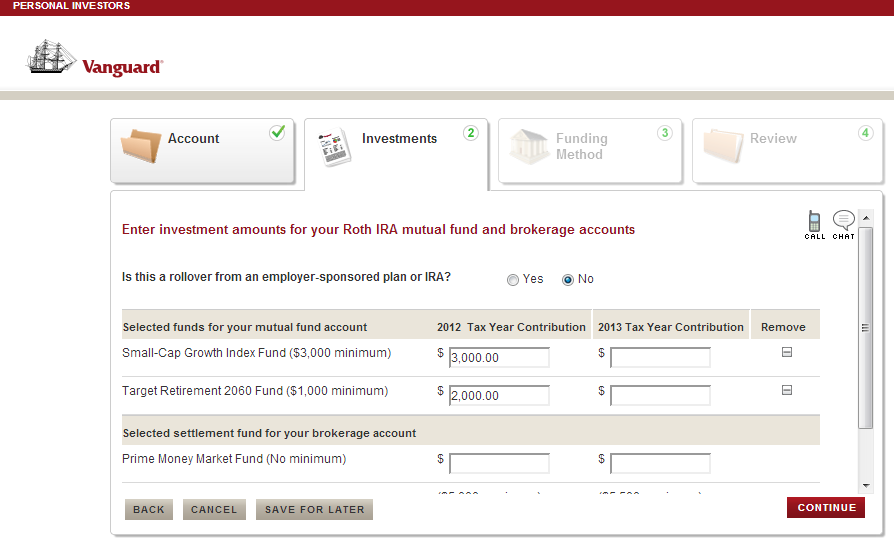

You’re not ready to select all of your investments?

Your money has to go somewhere even if you don’t want to invest it right now, for example in my case when I open up accounts for Mrs Saverocity I would check this option, deposit the full amount (only for 2013) into a Money Market Fund which is very stable until we sat down and discussed options on where she would like to allocate the funds. I wouldn’t decide to fund 2014 now, even though I could since I have until April 15th 2015 to make that decision. I may decide that this year I would rather deposit into a Traditional IRA or something else. I think it is likely that I will pick ROTH again, but I don’t think it is necessary to make that decision now.

Ready to Invest and Allocate your funds right now?

I opened up an account for both Mrs Saverocity and Myself today, for my own account I was ready to pick some funds and get going with the investments. This can be quite an aggressive move as you are faced with immediate asset allocation requests which I think is a little intimidating. Therefore if you are not certain where you want to allocate, but do want to set up the ROTH IRA before the deadline of April 15th then select the Prime Money Market Fund and park the money there whilst you consider which funds fit your needs.

Minimum Deposit for a Fund $3,000

Most of the funds on offer are asking for a minimum of $3,000, so if like me this is your first investment in a ROTH and you have the maximum $5,500 to play with this doesn’t leave you a lot of options for diversity (well, other than the fact that you can buy the ENTIRE MARKET with one fund). You are basically limited to picking one fund, or perhaps two, as there are some that allow a $1,000 minimum. I selected Small Cap US and a 2060 Target Date Retirement fund (for the latter, it is balanced between stocks and bonds, and I am no way targeting 2060 for retirement, I just want an aggressive, yet diverse mix to balance up some of the risk in selecting a small cap for my primary fund.

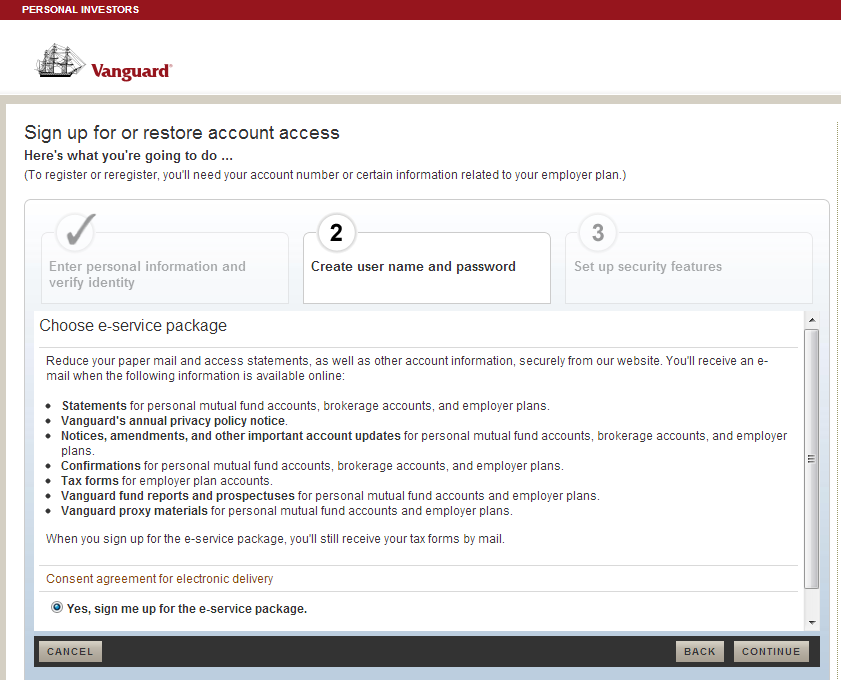

After a few more steps, that is basically it, your account is funded either by check or bank account, as mentioned before I picked bank account because that time-stamps my account opening for today and I don’t have to worry about any issues with the check not arriving or whatnot.

After you set up the account, you will then be prompted to set up online access. I do recommend that you do all this now, and e-sign the forms required by NYSE etc regarding your accounts. An important step here is to sign up for e-delivery too, this will save you the $20 account management fee for balances under $10,000. The nice thing is that this is just Step 2 on the online access setup, so it leads you through this step without having to hunt for E-Delivery.

Some Interesting Facts About Vanguard that I didn’t know

Vanguard is well known as the proponent of Passive Investing methodologies as championed by their Founder and Former CEO John Bogle, when you are told that Vanguard is the ‘best way to invest’ it is probably because people are trying to get you to avoid the heavily loaded mutual funds out there. Vanguard funds are thought of as Passive Funds, and no Load funds by most people (at least by me in any case).

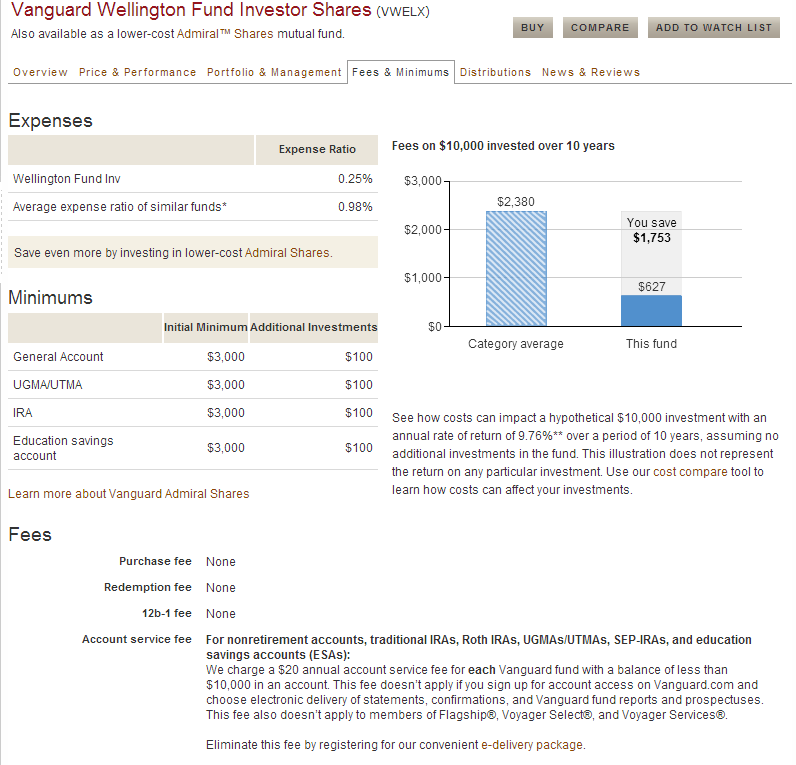

1. Vanguard has 67 Actively Managed Mutual Funds

This isn’t a new thing either, one of their funds the Vanguard Wellington Fund Investor Shares (VWELX) was created in 1929. However it was news to me. I had always heard the anecdotes ‘buy Vanguard Funds, they follow the Bogle principle of Passive Investing.. but apparently they do not, so be careful when picking your fund of choice that you know what you are buying into. The good news is that whilst they are an active fund, the price for ownership remains very low compared to the Industry standard. However it is worth noting that this management expense fee doesn’t include one thing that will impact an Active Fund more than a Passive Fund – Capital Gains Tax. It is assumed that Short Term Capital Gains will be higher when a firm is traded Actively, since they will be liquidating positions more frequently.

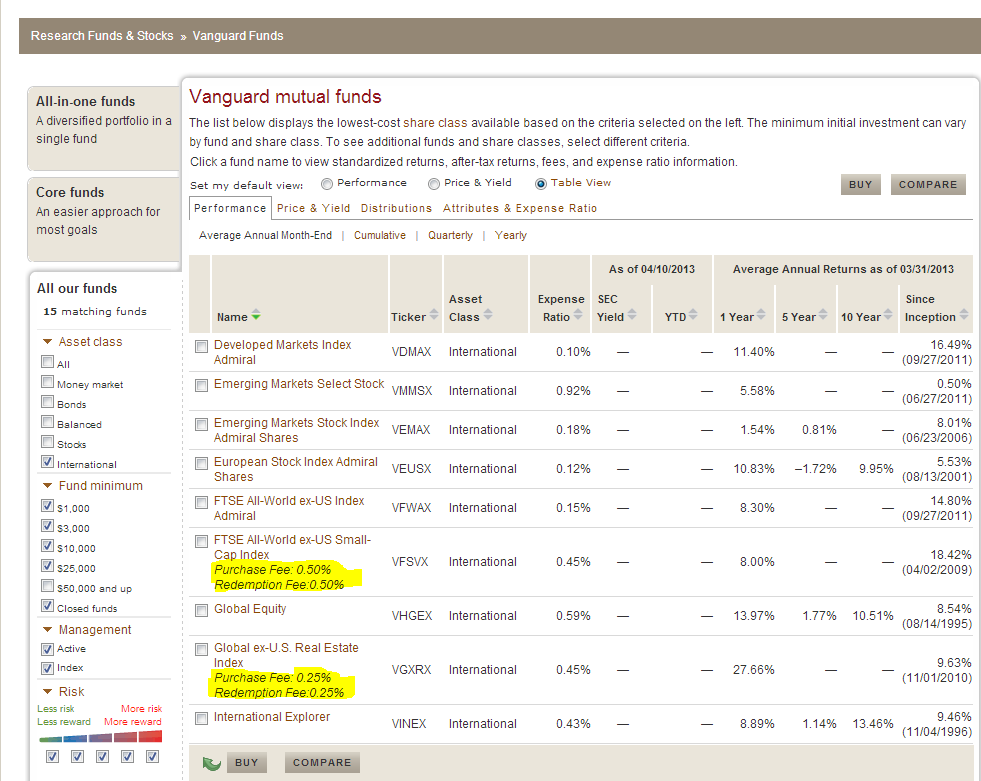

2. Vanguard Has Load Fees

Only on a couple of Funds admittedly, but I was very surprised to see a load fee and redemption fee. You can certainly see some that are a lot higher than this in the market with other firms, but I had always thought that this was something that you would never see with Vanguard. Also note that these funds have a higher (than the mean) fee than other Vanguard funds.

3. Vanguard Offers 3 Levels of Service for your Account

- Self Directed Accounts are managed by you, but do have access to support online and on the phone. I spoke today with a very nice and knowledgeable person from their Concierge service who really knew his stuff. This service comes as standard with any account at Vanguard, but don’t expect them to be proactive about contacting you regarding your account. This is more of an advice line.

- An Investment Management Consultation, this will give you a chance to talk with a professional to examine all of your accounts and assets and form an investment plan with their guidance. They charge for this service, and if you have less than 50K invested it will cost $1000, over $50K will be $250 and over $500K with them it is complimentary.

- A Managed Account – this is the highest level of service from them, where you basically hand over control of the account to Vanguard and they allocate accordingly, I tried to learn more about this from Concierge but he was a bit hazy, he mentioned that you might have to relinquish control of the account for a year at least to let these guys run it. Personally that makes me a little uncomfortable. Fees for the service are 0.7% for the first Million, 0.35% for the Second Million and 0.2% for amounts above that. Frankly, that’s too high for me now that firms like Betterment are offering that service for half of those rates.

4. Vanguard Blocks Fund Re-entry for 60 days

In order to keep costs low Vanguard discourages hopping around from fund to fund and in order to enforce that they lock you out of a fund for 60 days after you close the position. So if you are in Total Stock Market, and panic and decide to shift into Bonds then you cannot go back to the Total Stock Market Fund for the 60 day period, after which you can. It is worth noting that you can always exit and sell any position but they restrict you jumping back in, in order to discourage you jumping out. Further to this Vanguard now offers a lot of funds that are very similar in nature, and also ETFs that are very similar and don’t have this restriction. Whilst this may seem like a negtive, the restriction is actually helpful to you if you plan to Capital Loss Harvest in a Taxable Account, as you need to stay out of the same fund for 61 days to be safe – read more about that here Capital Loss Harvesting for the Index Investor

Despite a couple of quirky things as mentioned above, I think Vanguard is the best place to put your money if you are OK with rebalancing and asset allocation yourself (for more on this subject see this post: Portfolio Rebalancing for Passive Investors

Whenever you start setting up new Accounts I would recommend using a Portfolio Analyzer to check your current allocation to ensure that you aren’t paying excessive fees for any other legacy funds you might be holding, and to make sure that you are balanced out properly. Here is a review of the tool from Personal Capital that does a fantastic job of this – you should check it out even if you aren’t ready to open up something new now, as it will give you a snapshot of all your accounts easily, here is my review of their product:

Personal Capital Powerful Free Tool To Examine Your Investment Accounts

Hey Ed, sorry I missed this comment. Active traders means people who frequently buy and sell positions. Many of these swing traders will take the same stock, such as Ford and buy it and sell it when they think the timing is right. Vanguard is a believer in passive investments, which don’t swing trade to time the market.

Great post thank you. Began the application process and it seems that they do require you to select at least one fund before you can open the brokerage account for etf trades etc.. I assume one of their 1000 dollar funds (star fund, target retirement date etc.) would be sufficient. So for those with less than 1000 dollars to begin your roth it looks like Vanguard won’t work. If I’m incorrect on this please let me know 🙂 Thanks again.

You are correct, $1000 for the Target Date or Star Funds and $3000 to open a Money Market that allows access to the Brokerage accounts. I’m going to write a follow up post for people with less than this to invest.

Look forward to your post. The $3000 minimum for the Money Market required for brokerage accounts is actually only for new Vanguard customers. I was told this by a Vanguard rep when I called about the apparent disparity between your 3rd and 4th screen shot. I was able to open Roth accounts at Vanguard with $1000 total with both a Target Retirement Fund and their VBS brokerage service. I did this by following your instructions above and only selecting the “Vanguard Funds” option in step two. Then, once the customer relationship had been fully established (funds transferred etc), I added a second Roth account under the same login with the “brokerage account” only (note: I saw no option to add VBS to the existing Roth account online. From what I understand, a second Roth account is required due to VBS being structured as a separate entity from the mutual fund company). I have successfully made ETF trades in the brokerage account to supplement the Target Retirement Fund. I have not yet transferred money between the accounts. I also had to manually add the electronic delivery option to the VBS account. In conclusion, you can establish a Vanguard Roth with access to their mutual funds and ETFs with as little as $1000.

Ah I see, excellent news! The disparity in this post comes from the fact that I opened up two accounts here, one for me and picked my asset allocation at time of opening, and one for the wife. I wanted to sit down with her and have her pick her own allocations, so I put $5K into Money Market for her.

The good thing with the Brokerage account is that you can trade those Vanguard ETFs fee free, so they do allow access at an earlier level to investors with smaller portfolios. Plus their management fees average very close to their top level funds, that typically require $10K to enter.

Congratulations! I, too, am planning to open a Roth IRA with Vanguard and transfer an existing Roth ASAP from another custodian whose investment options and fees leave much to be desired.

Another argument against active trading in an IRA of non-Vanguard investments is that (according to a phone discussion with Mr. Chris Goudy at Vanguard a few minutes ago), any brokerage transaction fees are deducted from those precious and limited IRA assets. You cannot be charged for them separately. It’s best in that respect to stick with your original decisions as long as they make sense. Vanguard mutual funds and ETFs can be automatically reinvested (you can also direct dividends into the IRA’s associated money market account for reallocation if you choose). I’m not yet sure about others. Even if they inherently offer a reinvestment plan, check with Vanguard rather than assuming that you will be able to use it.

If and when you have further investments in a taxable account and are looking at the big picture, many advise keeping as many of your taxable bonds, and other relatively high income producers, in your Roth as possible, to avoid taxable ordinary income. The returns on long-term capital gains are taxed at a lower rate, so that the benefit of having them in an IRA is less. You may eventually reach the point where funds such as Wellington in the IRA, which comprise both stocks and bonds, are no longer the optimal choice.

Some great points here – certainly keep anything that isn’t inherently tax advantaged (like Munis) in a tax sheltered account such as the ROTH or Traditional IRA to protect your earnings.

This was so helpful, thank you! Couldn’t find anything else up-to-date!

Thanks Cathy, glad it helps. Let me know if you have any other questions about the account I can help with.

I think for those who want to actively trade, a dedicated brokerage account would be better because they have better rates (i.e. OptionsHouse, TradeKing). Love Vanguard because it’s really easy to see their expense ratio unlike some other companies where it’s rather difficult to locate that information. Also their “Price & Performance” tab allows you to easily see how a particular fund performs comparied to various benchmarks (i.e. S&P 500, DJIA, etc).

Yes, I have accounts with OptionHouse too, and it would be better for active traders, though most people don’t actively trade in their Retirement accounts, not that it is necessarily wrong to, providing you know what you are doing.

Does the initial 3000 dollars minimum to open an account counts toward the maximum amount you can put into a Roth account?

Hi Tom,

Yes it does. It is the IRS that sets the amount you can fund a Roth IRA in any one year ($5500 for 2013) and if you allocated $3000 in a Vanguard Roth IRA then you would only have $2500 left to allocate.

In theory you could put that balance of $2500 into a different broker, EG Fidelity, but that would get a bit messy, and in total you couldn’t put away more than $5500 ($6500 if you are 50 or over) unless you were taking the money from a Traditional IRA and converting it in. There is a way to do that that I outline here http://saverocity.com/finance/converting-to-a-roth-ira-using-partial-transfers-to-reduce-tax-costs/

My experience with Vanguard with an inherited IRA was the worst I have ever experienced in over 20 years as a private investor.

What should have been a simple, slam-dunk transaction ended up as a formal compliance complaint, a complaint to the PENN state attorney general, and my attorney at the ready.

The Vanguard “Transitions Team” was like dealing with a bunch of high school students.

Luckily, I documented every call, and they were on recorded lines.

You would think that they would have enjoyed a new six-figure account. This was “Kafka opens an inherited IRA with Vanguard.”

Sounds rough. To be frank, vanguard is as good and as bad as any other firm, they have the name in the market based on lowest fees and Bogles innovation of the Index fund but they are a firm like any other, which can spell trouble when you are dealing with something like you did.

I know you call it simple, but inherited assets can be complex, simply due to the complications that can arise when someone messes up. Hope you got it all straightened out now.

Sounds like you had a bad an experience as I’m having with a rollover from a Vanguard 401k due to a divorce. In addition to being laborious and time consuming, even when you pretty much fill in the blanks exactly as they ask you to on the QDRO, a lot of the agents are just plain rude. They really don’t seem to give a crap if you keep your money with them or not. I’d planned just to keep the funds at Vanguard and transfer my share of the 401k to an IRA, but I’m seriously reconsidering that after the ineptitude, foot dragging and lack of customer service I’ve encountered.

I, too, am having considerable difficulty getting funds transferred from my

ex’s Vanguard IRA to my Vanguard IRA account. Vanguard has all the

paperwork that was asked for in their “divorce kit,” but its been almost a

month and I can’t get any information out of them because its coming from

my ex’s account. Any tips on how you were able to get your transfer completed, Amy?

Very surprised to find so many positive review. I spent 20 minutes trying to reach their human customer rep, who does not even understand what 401k rollover means… I immediately switched to tiaa cref. I am very happy to have made a good choice.

Vanguard Customer service is poor.

Lousy customer service indeed.

I see that you opened two separate $5K accounts for you and your wife. Is this permitted for tax year 2013 if filing jointly with two income household and combined income under 181K? Thx!

I too am going to open a roth with vanguard…is this a better option than a traditional? and I was torn between the target funds and star fund…which would you recommend? Thanks!

Hi Rich, for the traditional vs roth that depends on your current income, if you go traditional then you reduce your taxes for this year, but defer them to when you distribute the funds in retirement – with a Roth you don’t get a refund now but the money grows totally tax free.

You just missed the deadline for 2013 so you have just under a year to decide which is best for 2014 contributions..

Hey Matt. Very useful write-up for confused beginners like me 😉 and there are a lot us out there. I was in the same quandary just a month ago, so wanted to share my experience too.

2013 was my first IRA. I have a 5 year old 401k account, so I decided to go the Roth IRA way, to kinda diversify my future tax liability. Could not start a well diversified portfolio with Vanguard. So instead of investing in a single fund or saving up in a money market holding, I decided to open a Roth IRA with Wealthfront. Since my portfolio is under $10k, I don’t pay any management fee. No trading fees or exit fee either, really a big deal for a small saver like me. They invested all of my contribution into 7 low-cost ETFs, which I couldn’t have achieved with Vanguard or even other houses like Fidelity or TD. In under a month, my account value is up 2% (unrealized, of course). What I don’t like about Wealthfront is that you cannot directly control what and how much you invest into (its “optimized” and automated based your risk score, and works for many people). I want my Roth IRA to round out my 401k, so I might move my IRA to Vanguard or a discount broker like Options House in the future.

I will write up a review of Wealthfront shortly. Their real value comes in when they implement tax loss harvesting (which doesn’t apply to IRAs) for account sizes over $100K

You aren’t in bad shape at all with them with an account size that you have, though I will note that you can trade ETFs with Vanguard for no fee (if they are within the Vanguard family of ETFs)

Set up may be fine, but transferring from Vanguard administered qualified plan to another qualified plan has proven well-nigh impossible.

I feel your pain. They have jacked me around for 6 months.

Hi Matt,

Yours Vanguard Index Funds review was helpful, but I’m very immature in this field and do not understand all very well. I’m 66 year old and will go to retirement for 1-2 years. I will be fine with my income for several years after retirement. When I retired I have to transfer 401K account to Traditional or ROTH IRA. Which would you recommend? Thank you!

Hi Borka,

I’m afraid I can’t tell you- there are so many factors to consider… If you search the site for IRAs and Roth that might help you.

When Vanguard charges .70% for management. When you say Betterment charges half that, that is misleading since their charge is for rebalancing. Not management. This is an apples to oranges comparison.

Hey Nick,

Not sure I agree with that. Can you explain what you get from management at Vanguard? I imagine it is asset allocation, with rebalancing. Which is the same as Betterment.

I see neither as a financial advisor – but am I wrong? Will Vanguard offer advice on paying your mortgage vs buying a fund, or talk to you about college planning?

I’m ready to be wrong, but I think they are pretty much the same thing here.

Matt,

Do have an email or anything that I can contact you on? I have a few questions about Vanguard that I would like to ask you if you do not mind answering them of course. Thank you!

Actually, disregard…I will just ask you on here …

I am torn between chosing a Roth IRA STAR with a risk level of 3 and Target Retirement Fund with a risk level of 4…Which would be recommended for just putting money away and not looking at it all for a few years? And which is going to get me better return in the event that I retire?

Hi John

Hard to predict the future, but to give you some understanding- in retirement the target date will be 65 bonds 35 stocks vs the STAR being 65 stocks 35 bonds.

Over time, the star will return more, but it will be more risky short term, as stocks fluctuate more than bonds.

Depending on your age, Star might be better but as a rule of thumb target date funds tend to work well, especially when looking to put away for years to come.

Hi,

I am 30 years old and i want to open my first roth IRA. I just need a 1000 to start right? do you think Vanguard is the best option for me? i want to contribute 5000 a year. I am very immature in this field 🙁 i need help!

Thanks

Hi Gabrielle.

Pardon me for jumping in before Matt had a chance 😉 I totally relate to your situation because I was there just a few years ago. Opening an account with Vanguard was not an option for me because they required a minimum investment of $3000 in each fund… which would not have got me a “diversified” portfolio. So I did, what I figured was the next best thing I could — I opened an account with Wealthfront. They need a minimum of $5000, which is all I had at the time, and it got me a diversified (well balanced) portfolio. If you want to start with a $1000, I would recommend Betterment (they have no minimum), which is very similar to Wealthfront with small differences — Wealthfront has no account management fees for accounts < $10,000, Betterment charges 0.35% (for < $10,000, and lower fees as your account grows) and requires an auto deposit of at least $100 a month. If you cannot do that, I would recommend Wisebanyan for you — they have no minimums and no account management or transaction fees. They only charge the ETF/fund fees which you will pay regardless of which brokerage you choose. They are best out there for someone starting out, in my opinion, and the only catch is — you have to get on a waiting list. But I can help with that. If you send me your email address, I can send you an invite which will get you to the front of that queue. (I get some kind of "referral benefit", not sure what that is, never invited anyone yet). I do not work for any of the services I have mentioned — I have accounts with Wealthfront and Wisebanyan. So there is really nothing in this for me, if you are wondering.

Welcome to the world of responsible investing — you are headed in the right direction. Oh, and Happy Holidays 🙂

Shaun.

This is good advice too- though with just $1k starting out the alpha from these firms isn’t really noticeable.

Vanguard is great. If you have nonotrr investments then you could look at a target date retirement fund, that will get you started.

So I am just starting a Vanguard Roth IRA. I was going to transfer 1000$. I’m 29 and get retirement thru my job but just wanted to have a separate account. Any recommendations? I have no experience in this field. I get the 20$ fee but what are other charges? I really don’t want to put in money when I’m not sure of anything

I opened a series of accounts with Vanguard– Vanguard has good products and a good website. It also has a horrific bureaucracy. I tried to move an IRA from another investment house. This is day 59 and still they have been unable to execute that seemingly simple maneuver. The people on the phone really do not know what is going on with your money. If you use them, you have to watch everything they do because they screw up everything.

I absolutely second that. My adult children inherited an IRA from their grandmother and after three months I am still not sure if Vanguard has set up the accounts, though I know they received the transfer from the other custodian. I spent over five hours on the phone with them just trying to get information as to what forms to fill out; the information given by three different reps turned out to be wrong. My son was sent a letter saying his account was set up but now (after the fact) he once again has to “confirm his identity” in order to access information about it. I’ve never experienced such ineptitude with any other company and I’m flabbergasted they get away with it.

and the worse part is that your money is NOT working for you for 60 days. I do not understand in this day and age that they claim that they have to wait 5 days from a transfer from another broker to “clear” before you have access to the funds. You know there is no paper check involved.

Yeah it isn’t ideal in your example… The key may be to invest in a Bogleheads manner within VG- in that you don’t trade regularly and if you are rebalancing you should never need to go to cash.

One of my problems with Vanguard is there is really no where for you to “park” your money. You mentioned that you transferred money into the money market fund, and then bought something else. But the money market fund also has the 60 day lock out period of when to sell. I also would like to transfer $500/month and when I hit $3K buy a new fund. There is no where I can transfer that “little” money. All I could really do is transfer into an fund I already have, then when I have the $3K, buy a new fund. But then that locks me out of the old fund for 60 days. I understand the 60 day rule, but there really should be somewhere I can park cash in my mutual fund account without jumping through hoops

Hi MAtt;

Per Gabrielle’s comments (December 23, 2014 at 6:06 pm) ; I am in the same situation where I have only 1000$ to start and the possibility to add minimum 5000$ at year; can you advise me if opening an account with Vanguard ( start 1000$) is recommendable and if it is, then which Fund will be or at list a good option you recommend?. I am 49 years old by the way.

Thank you very much

Al.

Hi Al,

I’d certainly recommend getting it in sooner rather than later as it has that much more time to grow. It is hard to say what exact fund to recommend without knowing what else you hold, and what your goals and risk tolerance would be. However, I would suggest that a Target Date Retirement fund might be easiest for you.

There are a bunch of funds at Vanguard, called target date 2030, 2035,2040 etc… if you plan to retire in 2030 that is your target date and it balances a mix of stocks and bonds for you. You can buy in for $1000. Note that the shorter the time to retirement, the less stocks and more bonds/cash you will see. That is because it is intended to be less volatile in retirement.

If you are aggressive, you can pick a further out fund, EG a target date 2050, that will give you more stock position, you can still cash that in at any time.. the date is just to indicate the mix of investments and isn’t a ‘must keep investment until this date’.

Hope that helps a litle.

Hi matt;

Thank you very much!, really appreciated your advise.

Best

AL

Yes…thanks Al & Matt…I too am 49 and trying to find out how to invest. So if I have 3k to invest, do I do the STAR fund for 1k and the other 2k for a target fund? How do I split up my 3k that I want to initially invest?

Cheers,

Dan

Again- almost impossible to answer without knowing a lot more about you- but I would just do the target date fund. Note that it can lose value as can any investment.

The strength is that it contains a mix of assets and ideally if one drops (eg stocks) the other (eg bonds) can repair the loss somewhat. The fund automatically rebalances itself in times like this, but still would see a short term drop.

Matt,

Thanks for the quick reply. Please forgive me about your comment “you need to know more about me?”….what exactly do you need to know. Here is the basic info…I have a 401k with Fidelity for 40k and a State Pension plan when I do retire. I’m looking for the best case scenario when I retire. I know that rolling over my 401k to a Roth IRA is not the best choice (online calculators and etc, unless I’m doing it wrong). So my mix for retirement is the 401k plan, State Pension, Social Security (doubt that will exist in 2030) and the Roth IRA…best option for an Roth IRA if you were in my shoes at age 49?

Thanks again for your time, appreciate more than you know.

Cheers,

Well the questions you need to ask are:

How much money do you need from the Roth? If your pension is enough to cover your retirement needs then you could:

a. Not need to risk anything in your Roth so go very conservative. (short term govt bonds)

b. Risk it all, because it doesn’t matter if the account drops as you don’t need the money. (all stocks)

The latter would mean 100% stocks and it could drop 30-50% in any year..

If you really DON’T need it then you can pick whatever you prefer from that.

If, however, your goals for retirement expenses are not met by your pension, what is the shortfall? That is a math question. How much do you need per month in retirement from this Roth?

You then take this monthly sum, say it is $200 and work out how much you need to save TODAY at what rate to achieve it. And you then fit an investment around those needs. If you don’t need 100% stock risk, don’t take it. But maybe you need more risk than short term Govt bonds.

That’s why it is hard to say specifically. You need your own numbers from your own expenses and future income. It can be done though, if you can figure out your retirement needs.

The target date option is the ‘safest’ in terms of suggestion as it has some risk from stocks and some stability from bonds and it balances itself. The weakness being that it is a little generic and we don’t know if it fits your own needs.

Hi, I am inheriting about $12,000 from my mom’s IRA which is in an Ivy Equity Fund with Merril Lynch. I’ve been reading about Vanguard Index Funds as good choices for IRAs since I am not an active investor. What would you recommend? In an inherited IRA, are you allowed to keep making monthly investments into it?

Hi Terry,

Index funds are great for keeping costs low, so would be a good idea. You also might want to look at Vanguards target date or lifestyle funds as they are low cost also (more expensive than a simple index, but still ‘cheap’.

You cannot contribute to the IRA, its a standalone account.

You can contribute to another IRA, inheriting one makes no impact on your ability to open another.

You must distribute the inherited IRA. You have 2 options: RMDs based on your age… IE it acts like you are already 70 1/2, but the amount of the RMD is based on your actual age. If you RMD this, you need the first payment distributed by Dec 31st after the year of her death. You need the IRS single life table for inherited IRAs for that. Alternatively, you can take a lump sum.

If it was a traditional IRA, the income is taxable under the rule of Income in Respect to the decedent. There is a deduction against this, but only if her estate paid estate taxes (only happens in larger estates).

If it was a Roth IRA and was opened for 5 years or more then the distributions are not taxable.

Hope that helped, let me know if you have other questions.

I am excited to find this discussion since I just open Roth IRA under my husband $5500 with $3000 going to vanguard index 500,$1000 to STAR And $1000 target retirement 2025 .

Matt , I hope this is a good idea and choice as far as what I choose above . I am new ! 🙂

I also opened another Roth under my name starting at $1000 and bought target 2035 and planning to deposit another $3000 in few days . I am trying to maximize $11k yearly contribution.

What do you think about the choices I made ?😁😁😁

Congrats on the new Roths! It’s hard to give detailed advice without knowing more about your situation, but if you have many years to retirement and are able to keep on contributing then you’ll likely be just fine.

Matt,

Thanks for super quick respond . We are 32 yo so I will be happy if we can retire in 20years to 25 years max . My husband already have deferred compensation through his work however I want to maximize our investment vs stashing cash on saving account .

do you think I should stick to this 3 funds and keep putting more and more yearly to maximize it or mix it with other fund that offered by vanguard . Example index 500 min purchase $3k so in 2016 I should add another $3k toward it and so on next year after or should I buy new investment for Roth ?

You need to look at everything all together- including the deferred comp plan and decide upon a mix of stocks, bonds and others that you feel comfortable with. The index 500 will likely gain (and lose) more than the target date funds… It really comes down to how much risk you need and want overall to achieve your life goals.

Thank you !:)

Hi Matt,

I am 28 years old and this past year decided it was time to start saving more aggressively for retirement. I have no real experience in this field but I have a former classmate who works for Northwestern Mutual so I decided to open a Roth IRA through American Funds. I have made 7 contributions at $458 dollars each month so I can maximize the $5,500 allowed each year. It is in a 2050 target date retirement fund. I have noticed that I pay a sales charge of 5.75% each month which equates to about 26 dollars. Am I giving away money? After some research it seems to me I could start a Roth IRA with Vanguard or someone else and have my money work for me rather than giving a portion of it away and stunting my growth. Would I be able to transfer the money I’ve contributed over the past 7 months to another Roth IRA easily? I also have a 401K through my employer but I’m trying to save through other avenues as well. Any advice you could give me would be great. Thanks in advance

Eric

Hi Eric, yes you are being robbed blind. Get out of that and into Vanguard!

You can rollover very easily, though you may get a fee from North Western to leave them too… I’d just get the hell away.

That’s what I thought, thanks for the advice I am calling Vanguard today

I am 66, semi retired, married, with a $26,500 pension. I have a $700K traditional IRA and I am not contributing anymore; I expect to collect my Social Security when I turn 70. When I turn 70 1/2, I have the RMD to contend with. My plan is to take $12K a year from my traditional IRA starting this year till I turn 70, and invest $6500 in a Vanguard Roth Index, and use the rest for home improvement.

My purpose is first, to draw down my RMD and the taxes, and second, to open a ROTH for both my children in their mid 30s. All this income is mine alone and does not include my spouse’s. Would this be a wise plan?

Hi Lorraine, it’s hard to say unequivocally if this is a good plan or not due to lack of other data, but the idea to suspend social security Til 70 is a good way to increase it (though perhaps it might be worth taking a spousal payment until then). Also reducing your RMD and funding a Roth can be a good idea, but also, it requires looking at the tax brackets of you vs your children, again, likely to be a savvy move but times when it might not be.

Overall, I’d say ‘probably’ looking good, but worth looking into married jointly tax brackets, spouses income, Childs rates etc in order to be certain.

Hi, I have a Roth IRA target 2030 lifepath for retirement with State Farm and I’m getting hit with huge fees to actively manage my account I was told I should go with Vanguard target retirement so my money grows have approx 6,500 in this acct. what are your suggestions? Also any input on American funds would be appreciated also. Be getting raked over the coals for years and my own fault but clueless on this stuff. Thanks

Yeah, get to Vanguard asap!!!

The objective merits of Vanguard and its products are well documented.

I will not keep more than a token amount of money at Vanguard however, because their customer service is inadequate. Their phone hours are far too limited outside of East Coast business hours.

Getting through to them during business hours recently has been beyond difficult. For example, after waiting an hour to speak to a person, that person transferred me to another department, where I just ended up in an interminable hold. What good is a brokerage that will not speak to its customers?

Hello. I am a 20 year old college student who is looking to open up a Roth IRA and was wondering if you can recommend what company to go with and how to start the overall process. I know that the minimum amount allowed to be deposited is $5,500 for those under 65 and also that people with income higher than $131,000 cannot contribute. My concern is what will happen to the money that I would have begun depositing in a Roth IRA account once my income surpasses the minimum amount.

Hey Harold

The min amount is $1. The max amount in a tax year is $5500 (under 65) you become ineligible on a sliding scale from $116k to 131k.

All it means is that if your income pops above the limits you can’t contribute to it in that tax year. Whatever is in the account is locked in and safe (other than the market movements of your investments) nothing happens to it if you later earn more. and if you later earn less (or limits rise) you can add another $1-5500 in each year.

Congratulations on the early start. I’m going to try to answer the part that Matt didn’t cover (perhaps because he doesn’t want to endorse any product/service? ;).

Unless you have good investing knowledge, I would recommend you start with a robo-advisor like Betterment or Wealthfront. My personal favorite is WiseBanyan. If you have some understanding of the markets, you could look at Motif Investing, a really interesting concept for trading.

Oh, sorry, I missed that part! Vanguard is fine. Robo advisors are ok, but their real value is in taxable, not tax advantaged 🙂

Hi Matt,

I currently have an traditional IRA with Vanguard, but am considering converting it to a Roth IRA. The balance is currently roughly $24k. Can I convert the entire balance after taxes or only up to a $5k limit? I look forward to your insight.

Thanks!

You can convert it all or part. Note that the amount you convert is included in taxable income so look carefully at your tax bracket and make sure you don’t convert at a high rate or one that pushes you up to the next income bracket

Matt–

Fantastic article, not only did I love your insight but I loved how helpful you have been with people who had comments/concerns. I have questions myself:

1) I am 22 and I just got my first full-time job. I make around $40K and my company offers a 6% match. My plan was to invest up to the point of the match into a Roth 401, and then max out a Roth IRA in either Vanguard or Scottrade (still debating which one, what do you think?). I want laid-back, passive accounts so I have been considering focusing both my future accounts in index funds. The problem is, I am not sure how to research and analyze the best index funds and I was wondering if you could steer me in the right direction? Mutual funds are very expensive, so would I be able to do indexes alone to get solid returns?

2) I understand a 401K has a $18K limit, so do you think investing up to my company match, and maxing out my Roth IRA is a poor move when I can strictly put it all in the 401? With that being said, I have student loan payments every month on top of both retirement accounts so I am trying to eliminate my debt while bolstering my retirement; so I was wondering your thoughts on that as well.

I am just a kid trying to self-educate himself, so your insight would be beyond helpful for me. Any sources, insights, information, and advice you could provide me with would be genuinely appreciated!

-Kurdt

Hey Kurdt,

Sorry for the delay getting back to you. First, it’s kinda hard to give proper advice without knowing everything, but based on what I see here I’d look into the following:

Roth 401(k) vs Roth = It would depend on the funds your 401(k) has access to – if they are good ones, then I’d just keep it there. Typically, the 401(k) has stronger protections in terms of creditor, which makes it slightly better than an IRA (depending on your state).

The one edge here might be that you are able to get a HSA (not FSA) from your employer – I may be tempted to take that after the 6% match, assuming premiums are affordable, as it allows for even better perks than the Roth if you use that correctly. Vanguard vs Scottrade.. Probably Vanguard. At this point you don’t have a lot of assets so you want to avoid transaction fees (buying the ETF may or may not cost money at Scottrade)

Student Loans might be the most important thing of all… the Roth offers tax free growth and withdrawal, but that is dependant on actual performance – IE you could put $20K into a Roth, and it becomes $10K. The student loan is a guaranteed rate of return – whatever you pay off from that is interest saved. It’s like buying a bond that pays a rate far higher than anything you could get in this low interest environment.

The last thing to look at is at $40K is there anything that you might have access to by going Traditional. I know most people say “you’ll earn more later..” but if you look at things like the Trad 401(k) or IRA to manipulate your AGI into ‘poverty zones’ then you can open up more free money, example of this is the Savers credit: https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-savings-contributions-savers-credit

Hope that helps with some ideas!

Thank you for the reply! I have another URGENT question!!

I am actually meeting with the 401K guy at my company tomorrow. My last question is the following: if I have a high probability of leaving my company within the next 3 years (vesting period), should I just do 2 ROTH IRA’s instead so I don’t lose my company match? What do you think is the smartest move to be in a lower tax bracket / to save the most amount of money long term!

You’re a life saver,

-Kurdt

Well a Roth won’t lower your bracket, so if that is the goal then the 401k will work to do that.

If you leave prior to vesting you don’t lose your own contributions, they are always vested, it is just the company side.

If you’re able to do a Traditional IRA based on income then that would work the same as the 401(k) in this case.

So overall, for my situation. should I just not do ROTH then? I prefer ROTH’s, but for tax purposes is traditional better? I guess I am foggy on how taxes work with both accounts. Like what would you say is the best move for my case.

Note: I also live in NY — incredibly high taxes.

I can’t tell you which is better from what I see here… but Traditional IRA and 401k lower taxes today (defer) whereas a Roth doesn’t impact today but grows tax free. Personally, I like to lower taxes when they are highest and receive taxable events when the bracket is lowest.

Thank you so much–

Just for a follow up I have decided to go with an Roth IRA, which I will max out for 2015 year before April. On top of that, I decided to go with a Traditional IRA with the company match, even though I will likely miss out on the match. Thought that would be the best approach. I should receive tax credits for the 8880 form you sent me with my AGI, so I thank you for showing me that as well. You’ve been more than helpful.

Hi I have 250k in Vanguard 2030 fund , also a 401k at work with no matching that I have 15% a week added to . It is with Wells Fargo in a Vanguard 2030 fund ! Wondering if I should lower my % to 401k and add more to my IRA ? I have 10 years till age 62 , what would be best Please ! Thank You

家

I’m 25 years old and I currently contribute 5% with my employer , they match up too 3%. I opened a roth ira last year and I only have $1200. My question is should I max it out the entire year . And also should i invest in the Vanguard Target Retirement 2050 Fund.