You are somewhat correct about the Roth. It seems that if you were to exclude your overseas income using the form 2555 FEIE then you wouldn't be able to contribute to a Roth unless your salary is in a real small sweet spot (above the exemption amount of $99,200 and below the cap of $116/131K where it phases out).

There seems to be one work around, but it shouldn't be considered in isolation. If you were to elect to take the foreign tax credit (form 1116) rather than exclude, it might create a situation where you are able to fund a Roth, but you need to realize that doing so will likely change the amount you pay in tax, and also will require that you itemize, which for many can be less beneficial than the standard deduction....

So, with that said, you could run the numbers and see what a 1116 credit creates for you, but it might be that you need to just not do the Roth for now.... but the reality is that many people can't fully fund 401(k), IRA and HSA from salary alone in the US, so if you build up a 'stash' of taxable income this can be used to fuel these accounts when you return.

Whether it is in the Roth or in a regular, taxable account, you should think about asset allocation and risk. You should think about worst case scenarios:

- If you invest in equities (stocks) they may drop 50% or more in any year.

- If you invest in bonds the current price will drop when interest rates rise.

- If you invest in CDs/Cash like accounts you won't make very much interest right now.

The best way to protect against the fluctuations of the market is to blend assets, have a mix of stocks and bonds. At a basic level, bonds are very consistent (but pay you less right now due to the underlying interest rate) and stocks are very inconsistent. So the more stock:bond ratio you hold, the more volatility you will experience - IE your account will fluctuate more. Think of bonds as anchors, that will keep things steady, however they will also prevent you reaching as high as pure stock allocations, while protecting you from dropping as low....

People talk about a lot of mixes here, you will here things like 80/20 or 60/40 portfolios (and anything between 0/100 or 100/0). The first number is % stocks, the latter % bonds The younger you are, the more you are supposed to favor the stocks side. For example, a person in their 20's might go for 80/20, 90/10 or even 100% stocks, whereas a person about to retire would likely have shifted this over time, and in the best case can be 100% cash and or some bonds and have enough money to retire without worrying about the market.

In terms of implementation I think it is important to write down an Investment Policy Statement (IPS). This should outline your approach to investing and should be your guide when you are in times of trouble... if you invest now, at some point in your future you will be in a market where your savings are down a lot, and you need to keep a calm head here. You shouldn't change the policy based on the market dropping, but you can certainly reconsider it based upon goals that will pop up on the way. IE if you have a kid, or if you are buying a home, you might want to look at your aggression levels for investments.

A cheap and simple solution to the IPS and the asset allocation is to commit to investing a fixed amount every month to an investment that automatically includes a blend of stocks and bonds. The name for these funds are Target Date Retirement or Lifestyle/Lifecycle funds.

Here's a list from Vanguard,

https://investor.vanguard.com/mutual-funds/target-retirement/#/?WT.srch=1

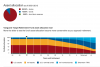

If you are 26 your retirement year should be around 40 years from today, so 2055. You can see that this fund by vanguard proposes you start with a 90/10 mix

If you look along the 'Years until Retirement' axis you will see that US stocks (in red) reduces, and bonds (in blue) increase as you approach and enter retirement. This fund takes care of that tweaking for you every year, so it puts you on a flightpath.

Additionally, if you find yourself in a stock market crash, the fund will automatically 'rebalance' itself by buying/selling to level out the stock to bond ratios. This saves work for you. What this means in general is that you buy the fund today, and 20 years from now it will have 'aged' with you, and your mix will be different. This type of investment requires little thought, has low cost, and good fundamentals.

A simple IPS might be "I will invest in a fund like this and deposit $X per month to it, regardless of the market 'noise'." You'll find that if you invest monthly, you will do really well via a concept of dollar cost averaging. Even if you invest next month and everything crashes, the next month invest again, and you're 'average' will be very good, and long term you'll do great. You can easily save up a few hundred thousand like this before needing to worry about 'optimizing'.

When you return to the US, you'll have a big nest egg saved. This is a time to be thoughtful. It is possible to now create a strategy where you can take all of these assets out of the fund without paying any taxes on it.