Dollar Cost Averaging is a quite well known method of investing that avoids the problems of trying to time the market. The basic premise is to add funds into an investment over a period of time.

Frequently the term is used to describe a long term savings plan, such as contributions to a company 401(k) plan that are taken from your paycheck on a monthly basis. An example 401(k) might have funds split into a basic 2 class structure of stocks and bonds, 80/20 between them. If you were to have a $1400 monthly payment going into the funds, each month they would buy:

The concept here is that with a consistent dripping of the investment your basis will 'average out' and you will be able to enter the market without the fear of buying high. The 401k style of Dollar Cost Averaging is more accurately known as a periodic investment strategy.

Dollar Cost Averaging Vs Lump Sum investing.

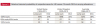

Dollar Cost Averaging is also a strategy used to drip a lump sum (rather than income) into the market over time. By setting a fixed period of time to invest it is thought that you would get in at a better rate. This is highlighted by this graphic by Vanguard:

This image, and variants of it are lauded by many financial firms as how DCA is a savvier financial decision, however it is actually a very biased data set, and used solely here to show how DCA works, when it works (IE should the price of later serial payments have decreased) if instead the value of the investment has increased then DCA is inferior to lump sum contributions.

So, in some ways you still have a game of guess work, but it does help facilitate a decision to invest when there is the fear of market fluctuations at play.

Should fear drive your investments?

Interestingly, the notion of DCA plays heavily upon marketing timing and fear. While it seems to present itself as a mitigation tool regarding such things, one could argue that simply acknowledging market timing is to fall under its spell. There is a very interesting article, also presented by Vanguard that proposes that DCA fails against Lump Sum Investing over three markets (US, UK and Australia) across a wide time frame: PDF Here

Chart from Vanguard

You have to get in at some point, the notion of drip feeding a lump sum comes with the downside of not having the balance invested in a meaningful investment. Furthermore, with each investment, as money moves from outside of the asset to inside of the asset the ability for the DCA to offset fluctuation decreases. And once the final DCA investment is made you have then lost all power, you are effectively in fully, and you no longer have the benefits of DCA going forward.

Repair Ratio

There is a ratio between a singular investment and the ability to repair it to par in the event of decline. The notion of DCA works along these lines, but eventually declines, and at this point investments need to shift from the core asset to a defensive asset class. Correlation is very important at this point, there is no value in selecting two assets that react in tandem to similar events if you are seeking to embed repair value to a portfolio. This is the premise behind diversification of assets, and it is something that you can explore in the comments, and I will extrapolate on in future posts. For now, let it suffice that diversification of assets too soon might be detrimental, but at a certain ratio of assets to income a repair variable should be implemented.

Frequently the term is used to describe a long term savings plan, such as contributions to a company 401(k) plan that are taken from your paycheck on a monthly basis. An example 401(k) might have funds split into a basic 2 class structure of stocks and bonds, 80/20 between them. If you were to have a $1400 monthly payment going into the funds, each month they would buy:

- $1120 of Stock funds

- $280 of Bond funds

The concept here is that with a consistent dripping of the investment your basis will 'average out' and you will be able to enter the market without the fear of buying high. The 401k style of Dollar Cost Averaging is more accurately known as a periodic investment strategy.

Dollar Cost Averaging Vs Lump Sum investing.

Dollar Cost Averaging is also a strategy used to drip a lump sum (rather than income) into the market over time. By setting a fixed period of time to invest it is thought that you would get in at a better rate. This is highlighted by this graphic by Vanguard:

This image, and variants of it are lauded by many financial firms as how DCA is a savvier financial decision, however it is actually a very biased data set, and used solely here to show how DCA works, when it works (IE should the price of later serial payments have decreased) if instead the value of the investment has increased then DCA is inferior to lump sum contributions.

So, in some ways you still have a game of guess work, but it does help facilitate a decision to invest when there is the fear of market fluctuations at play.

Should fear drive your investments?

Interestingly, the notion of DCA plays heavily upon marketing timing and fear. While it seems to present itself as a mitigation tool regarding such things, one could argue that simply acknowledging market timing is to fall under its spell. There is a very interesting article, also presented by Vanguard that proposes that DCA fails against Lump Sum Investing over three markets (US, UK and Australia) across a wide time frame: PDF Here

Chart from Vanguard

You have to get in at some point, the notion of drip feeding a lump sum comes with the downside of not having the balance invested in a meaningful investment. Furthermore, with each investment, as money moves from outside of the asset to inside of the asset the ability for the DCA to offset fluctuation decreases. And once the final DCA investment is made you have then lost all power, you are effectively in fully, and you no longer have the benefits of DCA going forward.

Repair Ratio

There is a ratio between a singular investment and the ability to repair it to par in the event of decline. The notion of DCA works along these lines, but eventually declines, and at this point investments need to shift from the core asset to a defensive asset class. Correlation is very important at this point, there is no value in selecting two assets that react in tandem to similar events if you are seeking to embed repair value to a portfolio. This is the premise behind diversification of assets, and it is something that you can explore in the comments, and I will extrapolate on in future posts. For now, let it suffice that diversification of assets too soon might be detrimental, but at a certain ratio of assets to income a repair variable should be implemented.

")