Ahh Twitter, it will send me to an early grave. I open links and want to scratch my eyeballs out. Today’s winner was XYPlanning Network with their favorite 8 Personal Finance blogs. Obviously I clicked it to see if they put me into pole position or if someone pipped me to that. What I saw instead was list of the Yakezie kids.

Why the rage? Well, really it’s two fold. On one hand we have XY Planning Network. Founded by Alan Moore and Michael Kitces, two serious guys in the planning world, it is a network of Fee Only CFPs that aim to provide GenXY planning. Love the idea, but don’t love the thought (or lack thereof) that went into the XY blog post today. A minor thing really, but at the root of something bigger for me.

The Personal Finance blogging industry is one that I hate with a passion. The reason for this is their target audience is people who are vulnerable. They are in debt, which comes from a lack of financial savvy, and they turn to blogs for support on getting their lives back together again. Instead, what we get are charlatans who are selling commission paying financial products in order to provide a lifestyle for themselves. Disclosures are murky, and some are not present at all. People are writing blogs and selling on their ‘integrity’ and every day another schmuck comes along. I hate this, and I hate when they are endorsed by a fee only planning network even more.

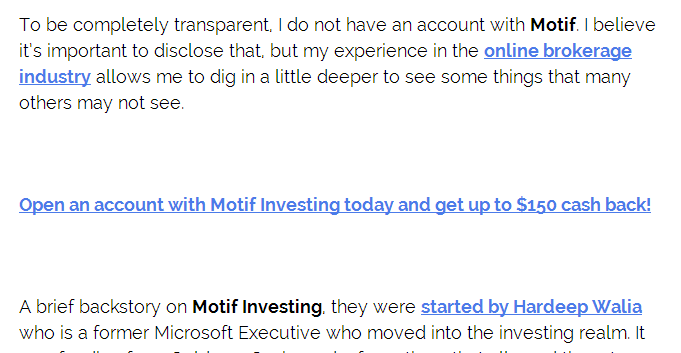

One of the blogs that caught my eye was Frugal Rules. I remember it from a post back in the day that was pimping a credit card without any disclosures in the post or clearly visible, I called John out on this and he said ‘he happy with his [lack of] disclosures. Now at least he does have a disclosure, as you can see in this Motif Investing post:

Disclosures to build trust, but omitting financial relationships and compensation.

‘To be completely transparent, I do not have an account with Motif..’ actually to be completely transparent how about: ‘I have never used this product and I make a commission if you buy it from me’. These sites are supposed to be about financial education and savvyness, and somehow that got lost once commission were being paid.

I thought to peruse the other 7 of the XY Planning networks top 8, and found 3 more with a similar approach:

#1 Afford Anything

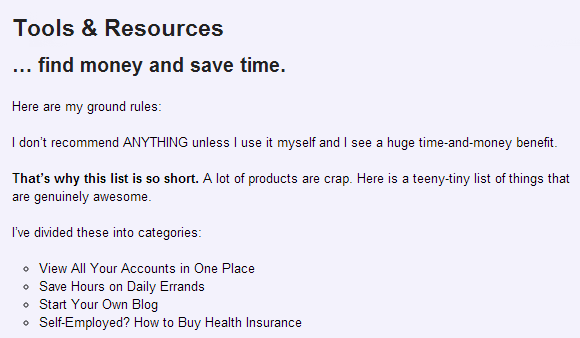

I thought the content was decent here, and no overly pushy affiliate links in the posts, for a moment I thought I was being wrong to judge these all because of “Frugal” rules. Then I checked out the ‘Tools and Resources Page”:

No mention of financial relationships, and everything recommended just happens to be a commission paying link. Coincidence?

Here are my ground rules:

I don’t recommend ANYTHING unless I use it myself and I see a huge time-and-money benefit.

That’s why this list is so short. A lot of products are crap. Here is a teeny-tiny list of things that are genuinely awesome.

I agree that a lot of products are crap, but the list here could equally be described as ‘here is a list of things that pay me good money if you sign up for’. That the author claims to use them personally is a great endorsement (and a great selling tool…) but again, where is the ‘Hey I make MONEY from this’?

#2 Broke Millennial

Not bad! A cursory look showed no affiliate links. There was a bit of pimping for the Plutus awards, but we all know that is being gamed extensively and needs all the promoting you can get! I have to say I can’t argue with this blog being in a good list for Millennial’s.

#3 The Empowered Dollar

It gets better! This blog is pretty cool, the author clearly spends time on it, and makes cartoons to explain financial matters- while I am not the audience for it, I have to give it props. Very little (if any?) affiliate stuff, and one sponsored post that was very clearly marked as such.

#4 Making Sense of Cents

I want to hate this blog, because it kinda fits into the Yakezie vibe, but when you look at it, its actually really good in the way it handles the money side of things, and I have to respect them for that. Affiliate links are clearly labeled, great to see!

#5 Young Finances

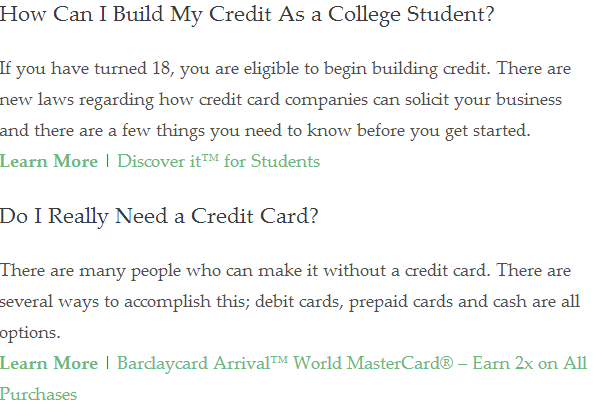

A big thumbs down for this one. They have a tab on the menu called ‘Credit’ – guess what, it isn’t about getting your shit together, its about selling credit cards, not a disclosure in sight. These two ‘questions’ are both lay-ups for slapping in the credit card link for Discover and the Arrival.

Check out credit – and get a card when you are at it (no card disclosure visible)

#6 Budgets are Sexy

Quite a popular site, and some solid content. No disclosures when they slip in affiliate links, noticed them for Amazon, and pretty links for other products.

#8 College Investor

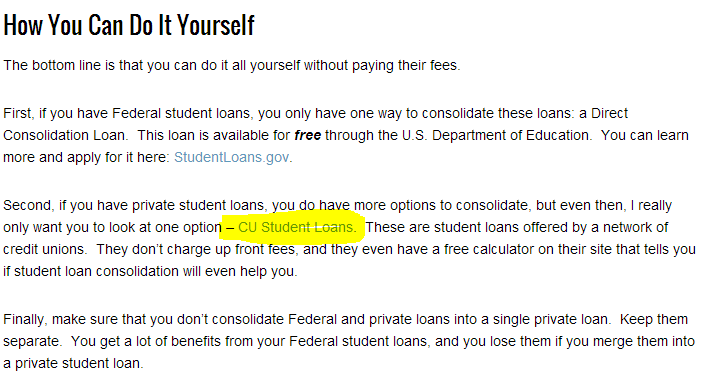

Overall was good, then I noticed they were slipping in affiliate links using ‘Pretty Links’, posts about sorting out your student debt, linking to loan consolidator companies. No disclosures.

Let’s slip in an affiliate link using pretty links, nobody will notice…

Conclusion

I don’t think it is fair to blame XYPlanning for including these in their list of top personal finance blogs, but I think if they are going to present themselves as a leader in the fee-only planning world then they need to be mindful of the advice that they offer to their customer base. The people I know who seek to be Fee Only planners do so because compensation source and conflicts of interest are top priority. They want to help people, these are the antithesis of these bloggers who seek to profit from their readers lack of financial awareness.

I really do hate this commercialization of the personal finance industry, and all the crap that comes with it. If you are going to start a blog to help people get out of debt then go for it! If you want to monetize that’s OK too, but once you start adding more and more affiliate channels in, and skip over the important points about disclosure and conflicts of interest, you enter a parasitic world.

The post Why I hate Personal Finance Blogs appeared first on Saverocity Finance.

Continue reading...