The Pattern is what I call the path of most efficiency, the order in which things should be done. Everything has a Pattern, here’s one you might understand and can apply to other things. For my morning coffee I sometimes have to wash a French Press. This means that I need water from the one tap in the kitchen. If I decide to wash the Press before filling the kettle my elected navigation is slowed by my own blocking of the pipeline.

In contrast, if I first fill the kettle with water, and allow it to boil while I am cleaning the Press, I’ve created an efficient Pattern. Effectively, I’m employing the kettle as an assistant, and outsourcing a role to it while I do something else. The coffee example is pretty fixed, it will always take 60 seconds for the water to boil, and 30 seconds to wash the Press. It is my choice whether the process takes a total of 60, or 90 seconds.

Some things are fixed in duration like the coffee and others have a variable nature. A variable pattern comes in with probability decisions. I use this for booking elaborate travel. I know that the airline seats are vastly more limited (especially when seeking 3 business class seats using points) than finding a place to stay at my destination. The rules surrounding the pattern are important.

- Coffee rules: water boil time, press clean time.

- Travel rules: value of plane ticket vs hotel room leans in favor of plane, and cancellation rules allow me to act faster and fix errors later.

- Age 30

- $80K Salary

- $20K living expenses

- $300K Mortgage ($1265 pmt)

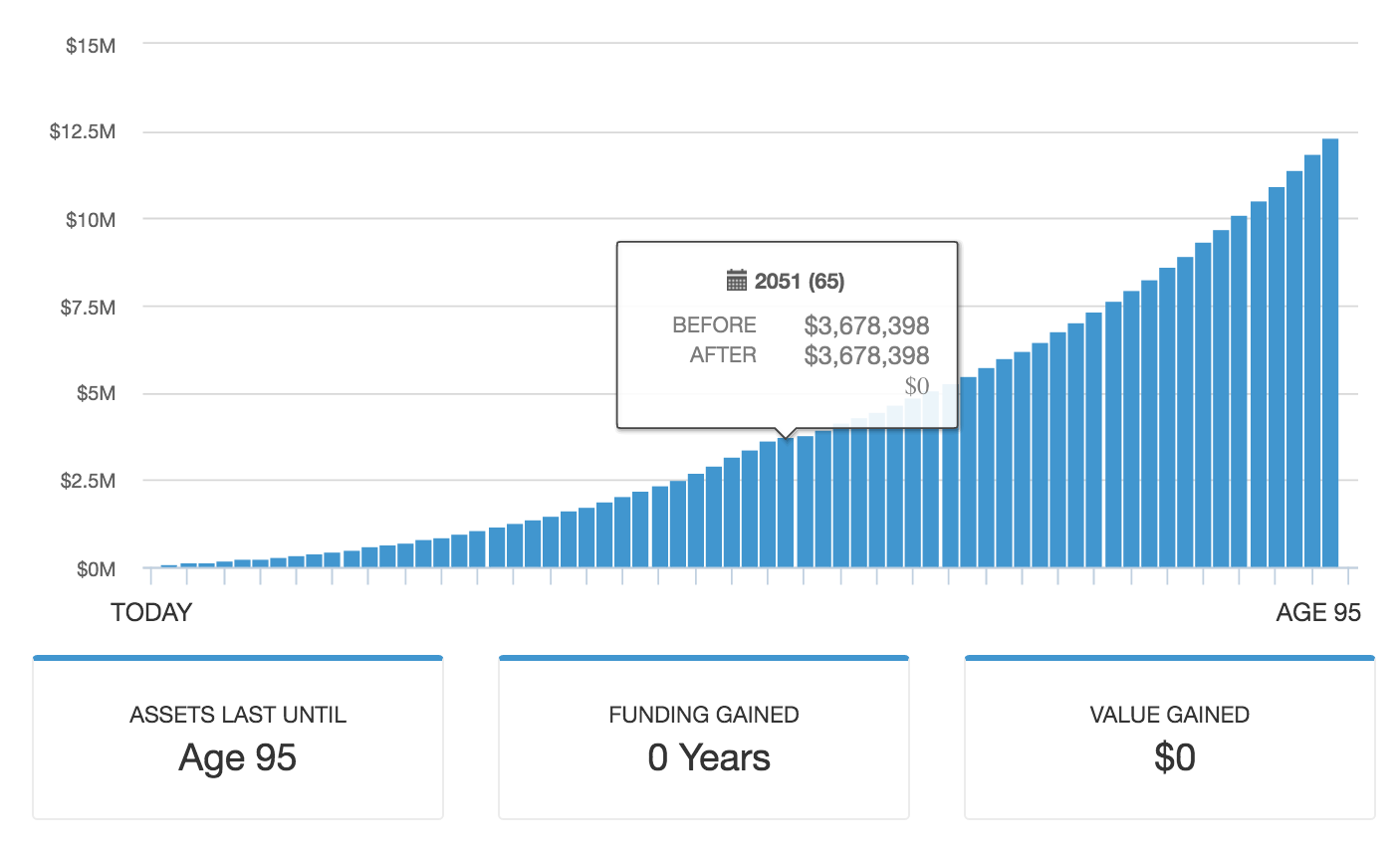

- $0 Brokerage Account

Brokerage Rate of Return 4.62% Pay mortgage monthly

Excess funds are invested in brokerage earning 4.62%

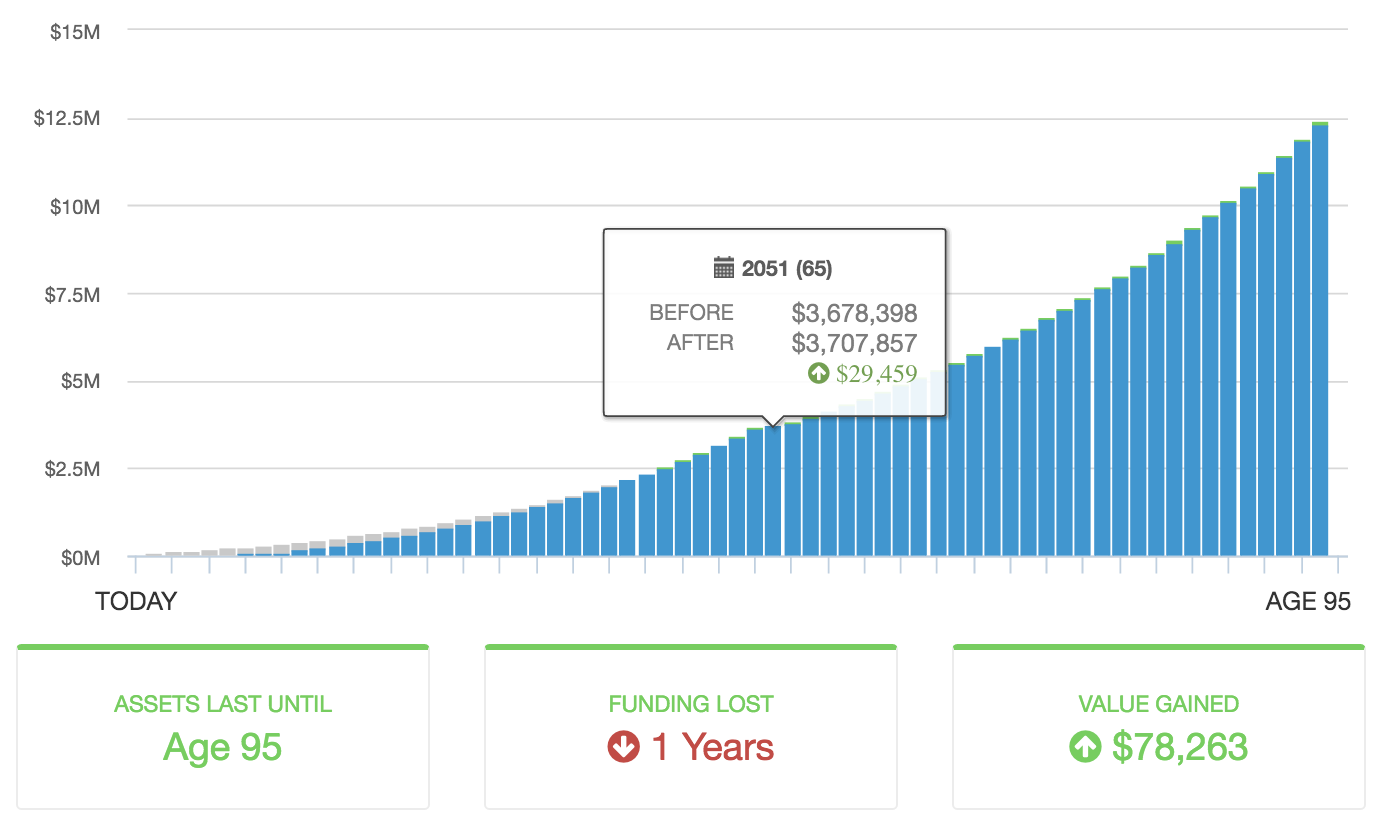

Compare that with scenario 2, where no money is invested into the Brokerage account until the mortgage is paid.

Making additional $25000 payments to mortgage

We get a lifetime gain of $78.263, and by age 65 a gain of $29,459. There’s actually some upside to paying off the mortgage at this level. However, if we swap the Brokerage rate of return to 7%, the following happens.

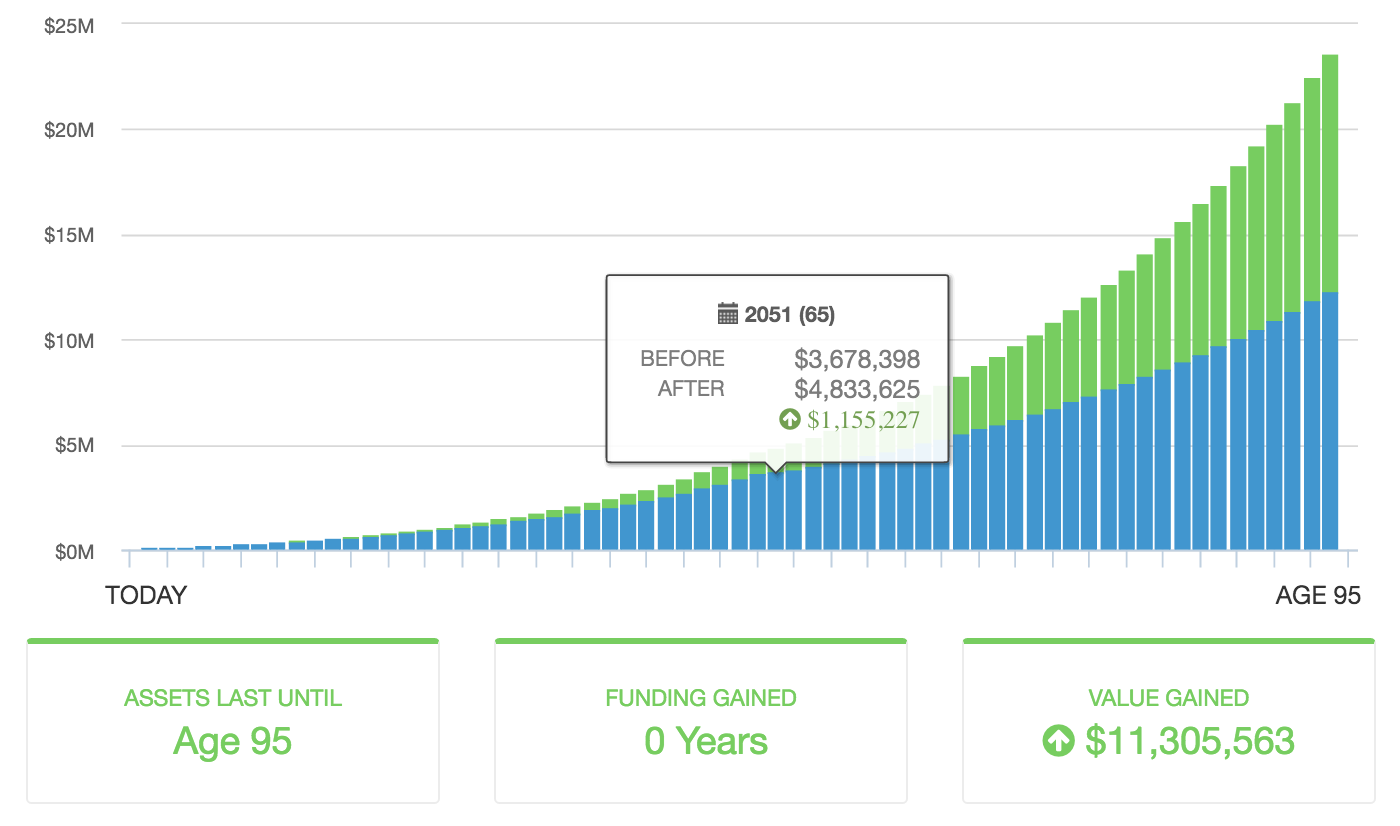

Brokerage Rate of Return 7% Pay mortgage monthly

Mortgage Pay Monthly Return at 7%

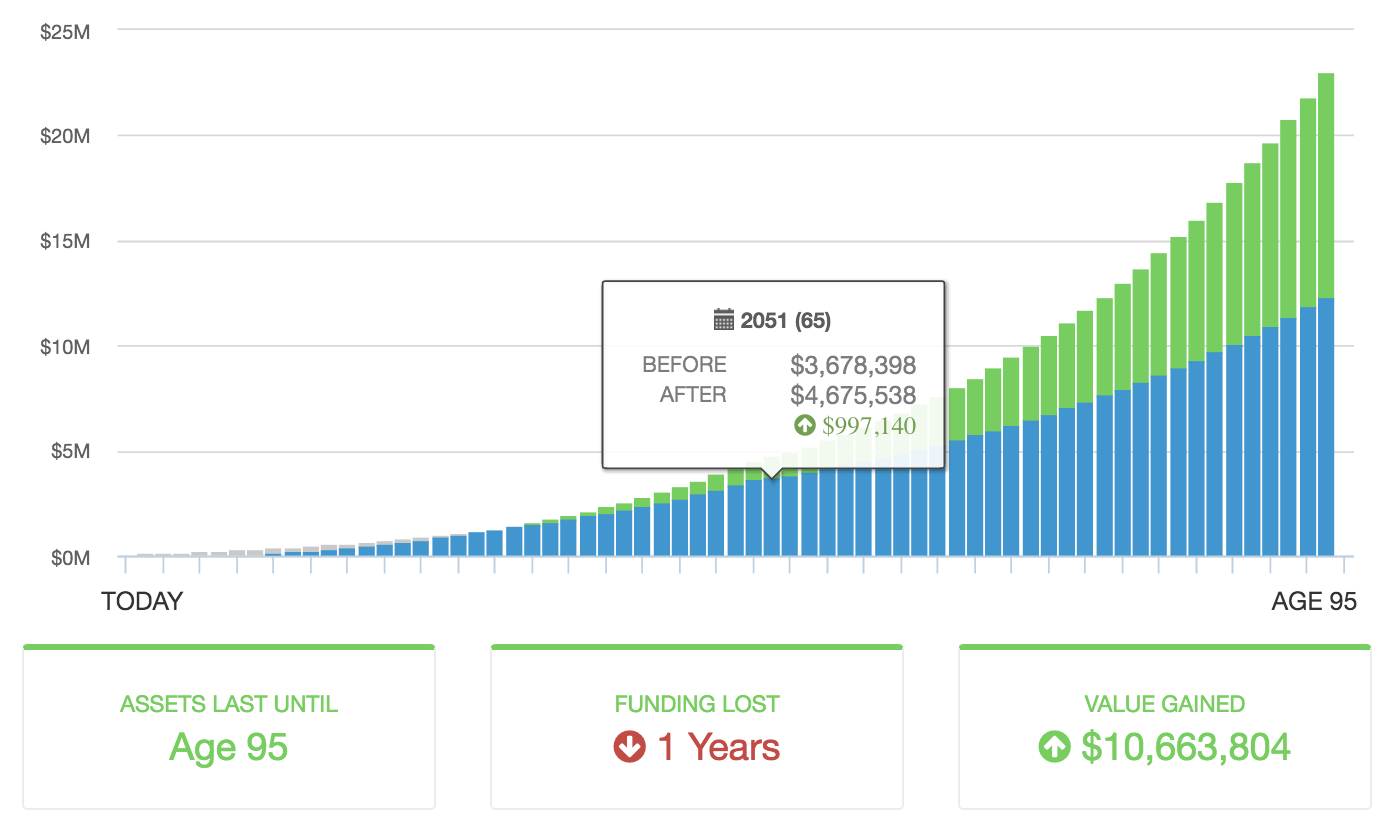

The increased rate of return from 4.62% to 7% creates additional portfolio value of $11,305,563. Whereas, if the person had elected to pay their mortgage early, their gain would be less:

No money invested in Brokerage until Mortgage Paid (7% brokerage rate of return)

Rate of return 7% but paying the mortgage first

As you can see, the pattern when the rate is 7% is clearly in favor of retaining the debt and paying the mortgage slowly, as you are borrowing low in order to invest high. This is the classic case of debt arbitrage at play.

However, what these charts are not showing is Probability of Success, which is very different from what you see above. Probability of success when the plan relies more on removing debt (a fixed rate of return) is higher than when relying on a variable rate of return from the market. When it comes to building a financial plan and thinking of the ‘Pattern’ many people forget the value of the probability aspect, and focus on the notion that a variable rate of return has historically produced a higher amount than the cost of their debt.

Probability when it comes to a financial plan is the key to everything.

When you look at various charts or models, keep this in mind as you decide on the Pattern, it isn’t what you ‘might’ get, but what is the minimum that you need to get with the lowest possible chance of it not happening. When planning in a more sophisticated manner, tax law comes into play. The relative valuation of a fixed liability in relation to a tax advantaged account vs a taxable account is different, so an order must develop. It might be that due to your tax bracket a 401(k) before paying debt is favorable, as the reduction in taxes creates greater cash flow. In another case, when income is low, and debt prices are high, it might be better to skip the 401(k) altogether and take the guaranteed rate of return first.

Patterns of most efficiency are everywhere. When looking for them remember that there are fixed and variable components. Try to visualize yourself being a manager, outsourcing roles. When it comes to the coffee, make sure someone is boiling the water while you are using it for something else, when it comes to debt, consider if your outsourced debt is working for you (in positive arbitrage) or against you, as real returns might not be at their historical levels.

The post The Pattern appeared first on Saverocity Finance.

Continue reading...