Lending Club and Prosper

- Thread starter Tom Juhn

- Start date

I personally wouldn't bother. I got in with a $1000 and it is growing well enough, but it really isn't a diversified investment IMO. I am re-investing the notes, but not sure how to exit profitably (am just letting it ride).

Here was my first post back in the day on Prosper: http://saverocity.com/products/how-to-find-and-fund-loans-with-prosper-com/ Which was in Jan 13...

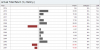

I'll log in now to see where we are:

So I am up 21% in 18 months... not bad I guess, but my issue is liquidity - I think I need to hit 'sell all' as a test to see what happens. They seem to have a second market for notes, but I don't know that I wouldn't get screwed on the spread.

I set up accounts like this all over for posts over time, but some annoy me more than others - this feels constricting to me.

Here was my first post back in the day on Prosper: http://saverocity.com/products/how-to-find-and-fund-loans-with-prosper-com/ Which was in Jan 13...

I'll log in now to see where we are:

So I am up 21% in 18 months... not bad I guess, but my issue is liquidity - I think I need to hit 'sell all' as a test to see what happens. They seem to have a second market for notes, but I don't know that I wouldn't get screwed on the spread.

I set up accounts like this all over for posts over time, but some annoy me more than others - this feels constricting to me.

Free-quent Flyer

Blogger

I can speak to the secondary market for notes. I needed some liquidity and was able to very quickly move my notes, without even pricing them very aggressively. I think I ended up netting 4-5%, much lower than the ostensible rate on the notes, but fine given that I was able to liquidate my position so easily (it took me 2-3 months to sell all the notes).

I call liquid 5 seconds.... That's a nightmare!I can speak to the secondary market for notes. I needed some liquidity and was able to very quickly move my notes, without even pricing them very aggressively. I think I ended up netting 4-5%, much lower than the ostensible rate on the notes, but fine given that I was able to liquidate my position so easily (it took me 2-3 months to sell all the notes).

Free-quent Flyer

Blogger

LOL it's designed to be a high-return, illiquid investment, I thought a few months to get out of a 5-year note, while still earning a few months interest, was pretty liquid all things considered.I call liquid 5 seconds.... That's a nightmare!

Made_by_Hugo

Level 2 Member

A couple of guiding principles and some rules.

Guiding principles:

- Some people won't pay you back; live with it

- People who have more debt are less likely to pay you back

- People with longer loans (5 vs 3 years) are less likely to pay you back

- People with less stable jobs are less likely to pay you back; state jobs and medical professions historically are the opposite

- People with mortgages on credit report more likely to pay you back

- Most people want to pay things, they just won't

Some rules:

- Don't lend to people trying to pay down medical bills - sad, but true, they are the highest risk of non-payment

- Don't lend to people with too much debt (30K+)- that's like giving a beer to your alcoholic friend

- Look for consistency in story - loan amount $20K but reported debt $12k? - consistent stories are the best

- Don't lend to people with spelling mistakes on posting

- Diversify, diversify, diversify - many small notes, different types of risk levels

- Look for people who are trying to refinance debt versus making purchase (ok trying to save a buck - makes you look savvy; if you paying for vacation but found Prosper and not the Saverocity forum, you shouldn't get a penny)

Guiding principles:

- Some people won't pay you back; live with it

- People who have more debt are less likely to pay you back

- People with longer loans (5 vs 3 years) are less likely to pay you back

- People with less stable jobs are less likely to pay you back; state jobs and medical professions historically are the opposite

- People with mortgages on credit report more likely to pay you back

- Most people want to pay things, they just won't

Some rules:

- Don't lend to people trying to pay down medical bills - sad, but true, they are the highest risk of non-payment

- Don't lend to people with too much debt (30K+)- that's like giving a beer to your alcoholic friend

- Look for consistency in story - loan amount $20K but reported debt $12k? - consistent stories are the best

- Don't lend to people with spelling mistakes on posting

- Diversify, diversify, diversify - many small notes, different types of risk levels

- Look for people who are trying to refinance debt versus making purchase (ok trying to save a buck - makes you look savvy; if you paying for vacation but found Prosper and not the Saverocity forum, you shouldn't get a penny)

Summerport

Level 2 Member

Wow, 13-14% return is excellent in my opinion.

I tried Prosper for 2 years and lost money.

I have done Lending Club for 3 years now and my average return is 6% with $5,000 invested and making pretty conservative picks. You're not going to get rich with these but I am happy with it, less volatility then the stock market and much better then money markets or CD's.

I tried Prosper for 2 years and lost money.

I have done Lending Club for 3 years now and my average return is 6% with $5,000 invested and making pretty conservative picks. You're not going to get rich with these but I am happy with it, less volatility then the stock market and much better then money markets or CD's.

See I don't know about that... its the less volatile bit that I disagree with, because I think the loans are less than ideal, and when doomsday comes they will default as fast as the market drops IMO. Further - if you look at VTSAX for 2013 it has a 33.52% return...(which is pretty wild in and of itself!)Wow, 13-14% return is excellent in my opinion.

I tried Prosper for 2 years and lost money.

I have done Lending Club for 3 years now and my average return is 6% with $5,000 invested and making pretty conservative picks. You're not going to get rich with these but I am happy with it, less volatility then the stock market and much better then money markets or CD's.

Miles Dividend MD

Level 2 Member

This is one of my least favorite investing strategies. I will steer clear of this and recommend the same to others.

I equate P2P to junk bonds with higher fees, more credit risk, and less liquidity on steroids.

I wrote about my objections in more detail here

http://www.milesdividendmd.com/sacred-cows/

Enjoy!

I equate P2P to junk bonds with higher fees, more credit risk, and less liquidity on steroids.

I wrote about my objections in more detail here

http://www.milesdividendmd.com/sacred-cows/

Enjoy!

thorax

Level 90 ( ͡° ͜ʖ ͡°) Warlock

I think they can have a (small) place in any diversified portfolio. Comparing them to VTSAX this year probably isn't fair. I started with 5k invested in Lending Club not too long ago. I think I'm averaging something like 12% returns. And with their automatic reinvestment bot, its fire and forget. I don't really need that money liquid anyway...

Ok- what is a fair benchmark for the risk profile of subprime loans?I think they can have a (small) place in any diversified portfolio. Comparing them to VTSAX this year probably isn't fair. I started with 5k invested in Lending Club not too long ago. I think I'm averaging something like 12% returns. And with their automatic reinvestment bot, its fire and forget. I don't really need that money liquid anyway...

I'm in, but I wonder how to get out

")

thorax

Level 90 ( ͡° ͜ʖ ͡°) Warlock

Yeah, I've no idea. But in theory if you diversify your (small) holdings over a multitude of loans, it might not be THAT risky.

edit: Surely there is some propellerhead here that knows how to calculation standards, means, deviations, hookers, blow, etc, right?

But in theory if you diversify your (small) holdings over a multitude of loans, it might not be THAT risky.edit: Surely there is some propellerhead here that knows how to calculation standards, means, deviations, hookers, blow, etc, right?

It's an asset class though- if you give $50 each to a crack head to only buy food how many will buy crack? Diversification within a flawed asset class is my worry- and doing so with less of a return than the market is my issue with it.Yeah, I've no idea.

edit: Surely there is some propellerhead here that knows how to calculation standards, means, deviations, hookers, blow, etc, right?

thorax

Level 90 ( ͡° ͜ʖ ͡°) Warlock

It's been awhile since I researched this, but if I remember correctly they have some pretty solid data back to something like 2005 or 2006. I know that isn't A LOT of data, but what they have shows consistent returns over that time period which includes a giant recession. Obviously its more of a gamble than buying a blue chip, but you're rewarded for that risk...

uchilaw13

Level 2 Member

It's been awhile since I researched this, but if I remember correctly they have some pretty solid data back to something like 2005 or 2006. I know that isn't A LOT of data, but what they have shows consistent returns over that time period which includes a giant recession. Obviously its more of a gamble than buying a blue chip, but you're rewarded for that risk...

uchilaw13

Level 2 Member

Kinda wrong re consistent returns during the recession; although 4 percent actual return for AA-B rated Prosper loans originating '05-'09 isn't the worst. According to the chart, though, nearly 18 percent of Prosper loans that originated during that time period and that were assigned retroactively a Prosper rating* defaulted. If you lump in all loan originated during that time period--whether they were retroactively assigned a Prosper rating or not--you're looking now at around a 19.3 percent default rate and a -5.66 percent actual return. That being said, a ton of investments were not doing great then.I've had a couple of beers. Does this mean I was right or wrong?

*From Prosper: "Loans booked prior to July 2009 did not have a Prosper Rating. Where applicable, Prosper Ratings have been assigned retroactively based upon our analysis of what the rating would have been at the time of the listing. Loans that were not retroactively assigned a Prosper Rating have been designated as N/A." My guess is that N/A is of a credit level so low that you couldn't even get a loan with Prosper these days.

MilesAbound

Level 2 Member

Liquidity is not tested in a bull market. "A few months" to get out of an investment in this market is absolutely horrible. I deal in far more complex and esoteric assets at work and in this market I can still shift most all paper in a month from waking up deciding I want out to being done. Shit I could put my house up for sale today and be done and closed in a month.LOL it's designed to be a high-return, illiquid investment, I thought a few months to get out of a 5-year note, while still earning a few months interest, was pretty liquid all things considered.

If it takes "a few months" now imagine how long it would have taken you in 2009? Probably would have had to take a huge bath.

Overall, this looks an absolutely shit investment to me (capped upside, lots of downside, shitty liquidity, opaque valuation) and as always I am guessing the guys making the money are the originators doing it all with y'alls money

Not sure if this has changed, but I was unable to get my statement from Lending Club's secondary note market (I think Prosper may use same platform) to upload to TurboTax a couple years back. Took forever to manually input what had very little impact on my overall tax burden and this, coupled with relatively illiquid market, was why I stopped trading on that platform.

Like some others here, my overall returns look pretty good, though I stopped adding to my account long ago and do not intend to start again.

By far and away my class of notes doing the worst are those where a bankruptcy was filed long ago. My initial thought was that those nearing 10 years since last bankruptcy were likely to see a credit score bump when the derogatory remark fell from their credit report and consequently the notes would then be worth more in the secondary market. Also, I figured that ten years separation from the bankruptcy was enough that it had little to do with the borrower's likelihood of repayment in the present. While credit scores did tend to see a bump upwards in the months following the loan, my portfolio of notes where the borrower had a past bankruptcy has a default rate 6x higher than any of my other portfolios (with a similar avg interest rate as the other portfolios). While I have been a bit lucky in realizing low defaults across my other loans and the sample size of the past bankruptcies was relatively small (20ish notes), my experience suggests it may be worthwhile to filter out borrowers with a bankruptcy in their past.

Like some others here, my overall returns look pretty good, though I stopped adding to my account long ago and do not intend to start again.

By far and away my class of notes doing the worst are those where a bankruptcy was filed long ago. My initial thought was that those nearing 10 years since last bankruptcy were likely to see a credit score bump when the derogatory remark fell from their credit report and consequently the notes would then be worth more in the secondary market. Also, I figured that ten years separation from the bankruptcy was enough that it had little to do with the borrower's likelihood of repayment in the present. While credit scores did tend to see a bump upwards in the months following the loan, my portfolio of notes where the borrower had a past bankruptcy has a default rate 6x higher than any of my other portfolios (with a similar avg interest rate as the other portfolios). While I have been a bit lucky in realizing low defaults across my other loans and the sample size of the past bankruptcies was relatively small (20ish notes), my experience suggests it may be worthwhile to filter out borrowers with a bankruptcy in their past.

Last edited:

DebentureBoy

Level 2 Member

I've been in both for several years. I was pretty enthusiastic at first, now not so much, but still in.

Pluses:

DB

Pluses:

- Easy. Set it and forget it (especially with Prosper)

- Can now deduct losses on taxes

- Some level of diversification (say, from stocks)

- Can do an IRA if you want -- eases the tax calcuations

- Taxes are a bit of a pain if you do it right

- Lower rate of return than what is advertised/reported... The math they use puts more weight on recent loans which have a lower default rate, therefore an artificially higher return

- IRA option doesn't allow you to harvest any tax losses

- Institutional investors are now very big into this. I gotta believe this drops the returns down in a few ways

- IRAs have to be two years in a row in order to minimize fees

- Unless they are held in an IRA, the income is taxed at your personal earned income rate

DB

thorax

Level 90 ( ͡° ͜ʖ ͡°) Warlock

@DebentureBoy Have you actually used the secondary markets with LC? I looked into it a while ago, but it just seemed like a giant pain in the ass.

DebentureBoy

Level 2 Member

Yes, I liquidated DW's LC account on the secondary market about a year ago. I did it in a three step process -- First I priced the notes at the market value (or some similar term -- essentially what the note was worth in terms of risk, return, previous payments, etc). I let that sit about two weeks and ended up selling a lot of the notes. Then I dropped the price by some percent (5%? I forget). That seemed to drop quite a few more fairly quickly. There were very few notes left at that point, so I "fire saled" them to just get rid of them. I'm a big time = money guy, so at that point it just wasn't worth it to try and maximize a return for a Chipotle Burrito dollar amount.

I wouldn't call it a pain. Obviously not something I would want to do all the time, but not a pain. I actually think a person could juice their return if they did this sort of thing more. It's just not the sort of thing I'm good at or enjoy, so I never pursued it.

I wouldn't call it a pain. Obviously not something I would want to do all the time, but not a pain. I actually think a person could juice their return if they did this sort of thing more. It's just not the sort of thing I'm good at or enjoy, so I never pursued it.

thorax

Level 90 ( ͡° ͜ʖ ͡°) Warlock

I just remember there was some alternate site you had to sign up for and it seemed like a pain. I dunno, I guess I should look at it again.

edit: I just went through the signup process. Seemed easy. I've no idea what I found hard last time. I'll assume that alcohol was involved.

edit: I just went through the signup process. Seemed easy. I've no idea what I found hard last time. I'll assume that alcohol was involved.

DebentureBoy

Level 2 Member

I MS better after I've had some alcohol...

Julian Brennan

Level 2 Member

After reading this statement a couple days ago I decided that it's really not the place I want my money to have. Especially the liquidity part gave me headache since I started putting money into LC. I'll just divert the incoming payments every month to other investments.I equate P2P to junk bonds with higher fees, more credit risk, and less liquidity on steroids.

I think some high class fixed income ETF with no load and low expense ratio will fit my personality better than a mix of 7-13% loans with a 1% expense ratio and zero liquidity.