Flanmann

Level 2 Member

Hi folks,

I was hoping you could critique my current investment holdings, and/or shed some advice going forward.

I'm 34, and I am an entertainer, so I travel from job to job, and don't have a 401K as an investment option unfortunately. I'm getting married in a few weeks, and looking to dive right into buying a house after. 75k income/year, no debts.

Here's what I have so far:

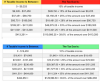

Roth IRA: appx 25k (I make sure to max this every year.)

TD Ameritrade Stock Acct: appx 20k

Savings (1.13% APY): 14k

Savings (0.9% APY): 3k

Mango Savings (6% APY): 5k, which I adjust accordingly to keep at this level.

I've left a bit more than I know I should in easily accessible savings lately, due to the need to pay various wedding bills. With the plan of buying a house within the next year, how should I adjust my current allocations of funds, or is there a new avenue I'm not using that I should get into? Any advice would be most gratefully appreciated.

I was hoping you could critique my current investment holdings, and/or shed some advice going forward.

I'm 34, and I am an entertainer, so I travel from job to job, and don't have a 401K as an investment option unfortunately. I'm getting married in a few weeks, and looking to dive right into buying a house after. 75k income/year, no debts.

Here's what I have so far:

Roth IRA: appx 25k (I make sure to max this every year.)

TD Ameritrade Stock Acct: appx 20k

Savings (1.13% APY): 14k

Savings (0.9% APY): 3k

Mango Savings (6% APY): 5k, which I adjust accordingly to keep at this level.

I've left a bit more than I know I should in easily accessible savings lately, due to the need to pay various wedding bills. With the plan of buying a house within the next year, how should I adjust my current allocations of funds, or is there a new avenue I'm not using that I should get into? Any advice would be most gratefully appreciated.